Virtual CFO Services for European SMEs: When Growing Businesses Need One

Nobody sets out to have messy books. It just happens. The financials become a pile of things you’ll sort out later. Then “later” arrives at the worst possible time.

End to end bookkeeping services fix that by taking ownership of the entire financial record-keeping process. Here’s what that actually means, what’s included, and whether it makes sense for your business.

The phrase gets thrown around, so let’s be clear about what it means.

End to end bookkeeping services cover the full cycle of financial record-keeping, from the moment a transaction happens to when clean, usable financial reports land in your hands. Every step in between is handled. Nothing left half-done.

Here’s what that cycle looks like in practice. A sale happens. Revenue is recorded. The invoice goes out. Payment comes in and gets matched to it. The bank is reconciled. Expenses are categorized. Payroll is processed. The accounts payable and accounts receivable ledgers are updated. At month end, a trial balance is run, journal entries are posted, and financial statements are produced.

That full loop is what end to end bookkeeping covers.

Contrast that with partial bookkeeping, where someone handles transactions but skips reconciliations, or runs reconciliations but never produces reports. Those gaps compound. By the time errors surface, they’re expensive to untangle.

A complete service also includes maintaining your chart of accounts, keeping your software correctly configured, and keeping your books GAAP compliant.

Not every provider covers all of this. Use this as a checklist when you’re comparing options.

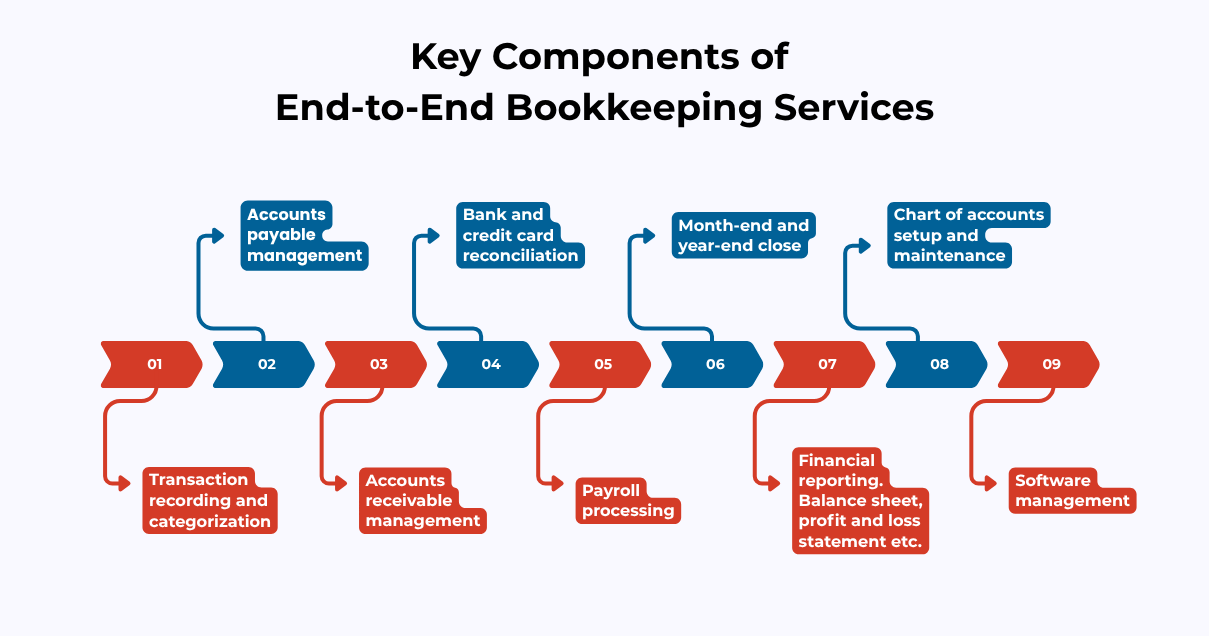

Transaction recording and categorization. Every income, expense, and transfer recorded and categorized correctly. Miscategorization distorts every report downstream.

Accounts payable management. Tracking what you owe, managing vendor invoices, scheduling payments. Good accounts payable management also helps you use payment terms to your advantage.

Bank and credit card reconciliation. Every account, every month, against actual bank statements. This is how you catch errors, duplicates, and anything that doesn’t add up.

Payroll processing. Tax withholding, compliance, correct amounts on time. Payroll processing is one of the highest-risk parts of bookkeeping when handled carelessly.

Month-end and year-end close. Accruals posted, books locked for the period. A clean year-end close makes tax season substantially less painful.

Financial reporting. Balance sheet, profit and loss statement, cash flow statement, and any management accounts your business needs, delivered within days of each month ending.

Chart of accounts setup and maintenance. The structural foundation of your bookkeeping. Get it right from the start and it holds up as you grow.

Software management. Whether you’re on QuickBooks, Xero, Sage, or FreshBooks, properly configured and used consistently.

The financial side of running a business has gotten more complex. Stripe, PayPal, Shopify, contractor platforms, subscription billing, foreign customers. Each adds a stream of transactions that needs to be recorded, categorized, and reconciled correctly. A few things tend to break down when businesses try to keep up on their own.

Cash flow visibility. Most owners are running their business off what’s in the bank account. That’s not the same as knowing your actual financial position. Your profit and loss statement sometimes tells a very different story.

Tax compliance. Whether you’re in the US, Australia, the UK, or New Zealand, tax authorities want accurate records. Tax preparation is faster and cheaper when books are maintained properly all year, not reconstructed in a hurry.

Lender and investor requirements. Clean accrual-based accounting records are non-negotiable when seeking a loan or outside investment. “We keep things in a spreadsheet” doesn’t hold up.

Decision-making. You can’t make confident calls about hiring or expanding without accurate financial reporting. Management accounts give leadership the numbers they need to actually operate.

Some of these might sting a little.

You don’t know what your profit was last quarter. Your profit and loss statement should not be a mystery. If you can’t answer that question confidently, something is wrong.

Bank reconciliations are weeks behind. Bank reconciliation is one of the most basic controls in bookkeeping. Skip it regularly and errors, and sometimes fraud, accumulate quietly.

Your CPA keeps asking for things you can’t find. If pulling basic reports takes days, your books aren’t in good shape.

You’re mixing personal and business finances. Once those lines blur, untangling them is painful and creates real problems at tax time.

You’re expanding into new markets. Multi-currency accounting, different tax rules, cross-border transactions. Not things to figure out as you go.

In-house bookkeeping means hiring someone directly. They learn your processes and are accessible on the spot. For some businesses, that proximity matters.

The tradeoffs are real. A qualified bookkeeper in the US, UK, or Australia is a significant salary before benefits. If they leave, you lose continuity. One person also rarely has deep expertise across payroll compliance, multi-currency reconciliation, and clean financial reporting all at once.

Outsourced end to end bookkeeping gives you a team instead of an individual. Different areas handled by specialists. Cost is lower. The service scales without hiring complexity.

With cloud-based accounting software, visibility isn’t a concern. You can see your books any time. A good outsourced provider keeps you informed, not guessing.

For most growing businesses, especially those with cross-border complexity or high transaction volumes, end to end bookkeeping combined with offshore bookkeeping services, this can provide better results, lower costs, and greater scalability.

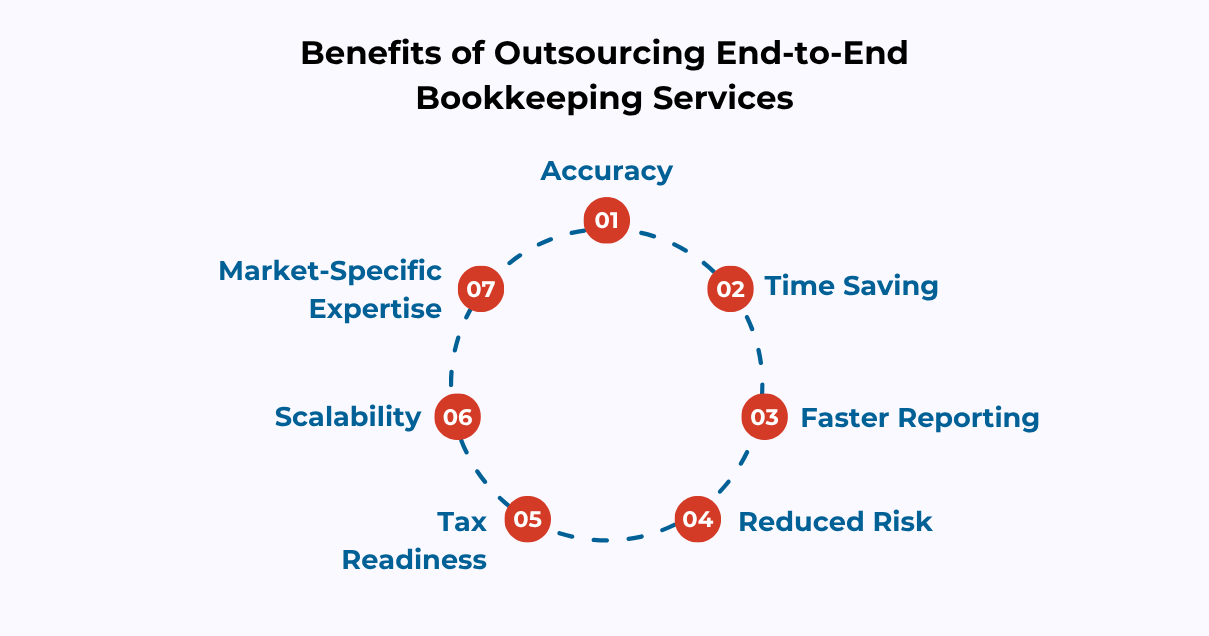

Accuracy. A dedicated team handles your books the same way every month. No gaps because someone is out sick.

Time back. For founders still doing this themselves, that’s often a substantial amount of time going back into the business.

Faster reporting. Reports ready within days of each month ending, not weeks. That timeliness changes how useful the numbers are.

Reduced risk. Regular bank reconciliation and proper segregation of duties cut the chance of errors or fraud going unnoticed.

Tax readiness. When books are well-maintained, your CPA spends less time on cleanup and more on strategy. Lower fees usually follow.

Scalability. The service grows with you without recruiting, training, or HR overhead.

Market-specific expertise. US GAAP-compliant accounting, Australian GST, UK VAT. Specialists bring what a generalist hire often doesn’t.

Keep business and personal finances completely separate. It’s the single most common issue we see when onboarding new clients. Fix it early.

Reconcile every month without exception. Monthly bank reconciliation catches errors while they’re still manageable.

Set up your chart of accounts properly before you grow. Restructuring it later, with years of data behind you, is a project nobody wants.

Choose the right software for your market. QuickBooks is dominant in the US. Xero is stronger in Australia, New Zealand, and the UK. Where you operate and where your accountant works should drive this decision.

Close your books monthly. Open periods create confusion and make reporting unreliable.

At Indian Muneem, here’s what working with us actually looks like.

Onboarding. We start by understanding your business. Revenue streams, expense structure, software, multiple entities or not. We review your existing books, clean up what needs it, and set up a proper chart of accounts for your industry and jurisdiction.

Ongoing transaction management. Transactions imported, reviewed, categorized, and matched regularly, daily or weekly depending on your volume. We work inside your existing software with no disruption and a full audit trail.

Monthly reconciliation. Every bank account, credit card, and loan account reconciled at month end. Anything unusual gets flagged and resolved before it becomes a bigger issue.

Financial reporting. Once books are closed, we produce your profit and loss statement, balance sheet, and cash flow statement. Custom management accounts built around what your business actually needs.

Collaboration with your CPA or tax agent. Specific reports, transaction detail, documentation for a filing. We get it to them quickly and in a format they can use.

Year-end support. By the time year-end arrives, your books are already in shape. Adjusting entries, final close, everything your CPA needs.

Professional services. Law firms, agencies, consultancies. Project-based billing means strong accounts receivable management and WIP (work in progress) tracking are critical.

eCommerce. High transaction volumes, marketplace fees, returns, refunds, and often multi-currency accounting. A solid setup here typically includes integration with Shopify, Amazon, or similar.

Real estate. Multiple entities, depreciation schedules, and loan accounts. This sector needs bookkeepers who understand how property transactions actually work.

Healthcare. Insurance billing, payroll across multiple staff categories, and compliance requirements. A team that knows the sector handles these without hand-holding.

Startups and scale-ups. You may not need a full finance team yet, but you do need accurate books, especially when raising capital. Outsourced bookkeeping is built for this stage.

CPA firms. Many accounting firms outsource client bookkeeping to specialists so they can focus on higher-value advisory work. Indian Muneem works with CPA firms across the US this way.

Trades and construction. Job costing, subcontractor payments, retentions, progress billing. Bookkeeping here tracks profitability by project, not just across the business.

We’re not a generalist outsourcing firm with bookkeeping on a service list. This is what we do, specifically for businesses in the US, UK, Australia, and New Zealand.

Our team includes Chartered Accountants and experienced bookkeepers who know both the technical standards and the practical requirements of your market. We work with US GAAP for American clients and understand Australian GST, UK VAT, and New Zealand tax requirements. US CPA firms outsourcing client bookkeeping will find we slot into existing workflows without friction.

We work across QuickBooks Online, QuickBooks Desktop, Xero, Sage, FreshBooks, and Wave, within your setup, not around it. You get a dedicated point of contact, monthly reports within five business days of the month end, and financial data handled with encrypted communication and strict access controls.

End-to-end bookkeeping services aren’t a luxury. They’re what any business that wants accurate financials, clean tax filings, and confident decision-making actually needs.

Businesses do not typically engage these services directly. Accounting firms use them to manage audit workload and documentation demands. The downstream benefit to the business is a more timely, better-documented audit.

We use cookies and similar technologies to improve your experience, personalise content, and analyse traffic. Some are essential for access to our products and informational resources. Certain services or pages may also be governed by additional Terms of Use. Manage your preferences at any time.