Xero Bookkeeping Services: How IMCA Helps Businesses Streamline Accounting and Financial Management

Table Of Contents

Toggle

CPA firms in the US, UK, Australia, and New Zealand are stretched thin. Not because the work isn’t there. Because the people to do it aren’t. Accounting graduates are declining. Experienced staff are expensive and hard to keep. And clients still want everything faster, cleaner, and cheaper than last year.

So, the firms that are actually growing right now? Most of them have quietly made a shift. They’ve combined AI in offshore accounting with qualified human teams. And the results are hard to argue with.

This isn’t about chasing a trend. It’s about solving a real operational problem with a combination that actually works.

Offshore accounting has been around long enough that most CPA firms have an opinion on it. Some have had great experiences. Others have been burned by communication gaps, inconsistent quality, or teams that just moved too slowly.

But the version of offshore accounting that firms are using today is genuinely different from what it looked like five or even three years ago.

The old model was mostly about labor arbitrage.You shift your high volume, low complexity work to a lower cost center. You save money, but you don’t radically transform possibilities.

The new model adds AI technology to this process. AI-driven data capture, AI-based reconciliation, AI-highlighted exceptions, and real-time reports. You’re not just saving money anymore. You’re delivering faster, more accurate work than a purely manual process ever could.

That’s what AI in offshore accounting actually means in practice. Not robots replacing accountants. A smarter delivery model that gets more done without cutting corners.

Worth being specific here, because the phrase gets used loosely.

At the basic end, it’s tools like machine learning-based transaction categorization that learn from historical data and auto-code entries. Most modern accounting platforms already do some version of this.

At the more sophisticated end, it includes:

Optical Character Recognition (OCR) technology which extracts information from invoices, receipts, and bank statements without any keying by humans. This single step cuts out an enormous amount of work involved in bookkeeping manually.

Automated bank reconciliation that correlates transactions between accounts within minutes and only highlights the discrepancies for human inspection.

Artificial Intelligence-based anomaly detection system that identifies duplicate payments, anomalies, or transactions outside the norm before becoming an issue.

Predictive analytics that offer foresight to our clients rather than merely providing them with hindsight.

When these tools run inside an offshore accounting team, the team’s capacity multiplies significantly. They stop spending time on data entry. They start spending time on review, judgment calls, and the work that actually requires a trained accountant.

That’s a fundamentally different value proposition from traditional offshoring.

Cost structure: A senior accountant in a major US or UK city, fully loaded with benefits and overhead, can cost $150,000 or more per year. A high-quality offshore team backed by AI tools can handle comparable output for a fraction of that. The margin difference is significant.

Scale during busy periods: Tax season hits and you suddenly need 30% more capacity. With a domestic team, that’s a hiring problem. With an AI-enabled offshore model, it’s much more manageable. You’re not onboarding new staff. You’re using a team and a system that’s already running.

Better deliverables for clients: When AI handles the transactional volume, offshore accountants can do more substantive work. Cleaner financials, faster month-end close, better management reports. Clients notice.

Competitive pressure: Some firms are simply moving because their peers already have. Early adopters of AI in offshore accounting are delivering faster and cheaper. That puts pressure on everyone else.

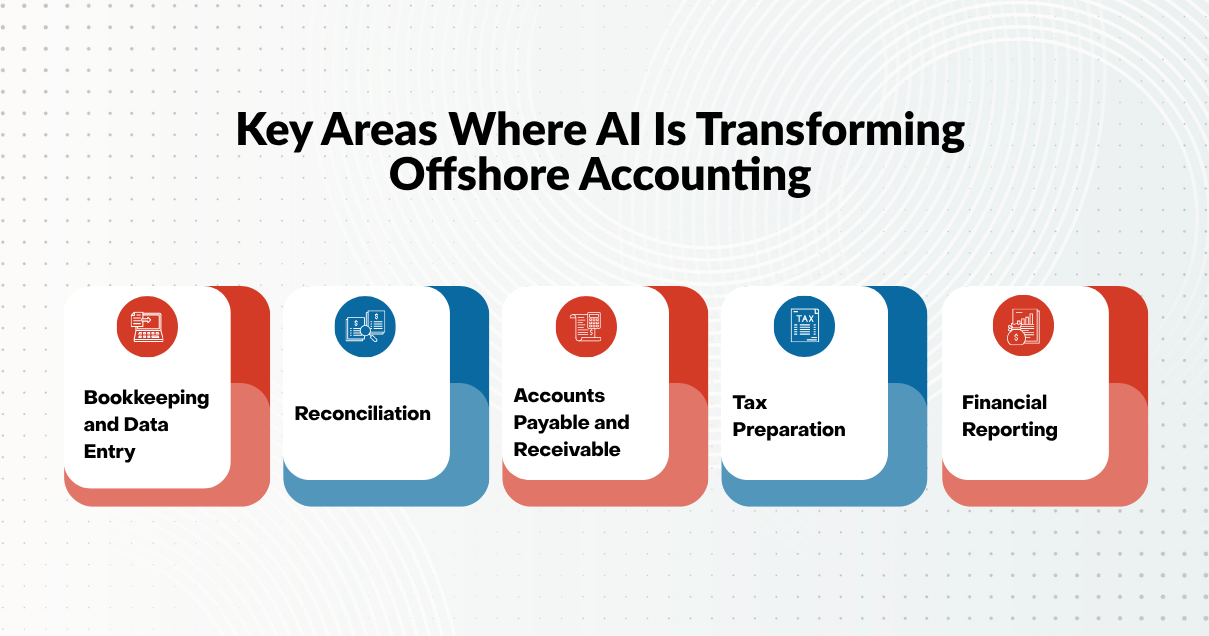

Not every accounting function benefits equally. But across the core services offshore teams typically handle, the shift has been real.

This is where the impact is most immediate. Automated data capture through OCR and direct bank feeds removes the manual entry step for the vast majority of transactions. Offshore bookkeepers are reviewing data instead of typing it. That’s a quality improvement as much as a speed improvement.

AI-powered reconciliation software processes thousands of transactions across multiple accounts in minutes. Exceptions get flagged. The offshore accountant handles the exceptions. What used to be a full-day task becomes an hour of focused review.

Intelligent invoice processing reads documents, checks them against purchase orders, routes for approval, and logs the entry. On the AR side, AI identifies overdue accounts and prioritizes follow-up. The human picks up where judgment is needed.

AI tools can pull financial data, apply current rules, calculate liabilities, and populate return forms. But tax compliance management still requires human interpretation. Tax law isn’t purely mechanical. The offshore tax accountant using AI-assisted tools does both faster and more accurately than either could alone.

Automated financial reporting compiles trial balances, generates standard statements, and drafts initial commentary. The offshore accountant reviews, adds client-specific context, and finalizes. Days of work become hours.

The “will AI replace accountants” conversation gets tiresome, but it’s worth addressing directly because firms make real decisions based on it.

AI processes data. Humans interpret what it means.

When a transaction is unusual, AI flags it. A human decides what to do about it. When a tax position is ambiguous, there’s no algorithm that replaces the judgment of an experienced accountant who knows the client, the industry, and how the relevant authority tends to interpret those rules.

Regulatory compliance expertise is inherently interpretive. Guidance from the IRS, HMRC, the ATO, or Inland Revenue isn’t always clear-cut. Applying it to specific client situations requires professional judgment and accountability. That’s a human function.

Client trust is also a human function. CPA firms compete on relationships. Clients share sensitive financial information because they trust the people handling it. AI doesn’t build that trust. People do.

The honest framing isn’t “AI vs. accountants.” It’s “AI makes accountants significantly better at the parts that matter.” The firms understanding that distinction are the ones pulling ahead.

Think of it as a division of labor built around what each does best.

AI handles volume, consistency, and pattern recognition. It applies rules without getting tired. It processes data at a scale no human team can match. It doesn’t have a bad day.

Human accountants handle judgment, client communication, professional responsibility, and the situations that don’t fit the standard workflow. They know when something technically correct is practically wrong. They ask the question AI doesn’t know to ask.

The AI-human collaboration in accounting that works best is one where neither is being asked to do what the other is better at. AI does the heavy lifting on data. Humans do the thinking on what the data means and what to do about it.

Firms that have implemented this model well report measurable improvements across the board. Faster turnaround. Lower error rates. More capacity for advisory work. Clients who are noticeably happier with what they’re getting.

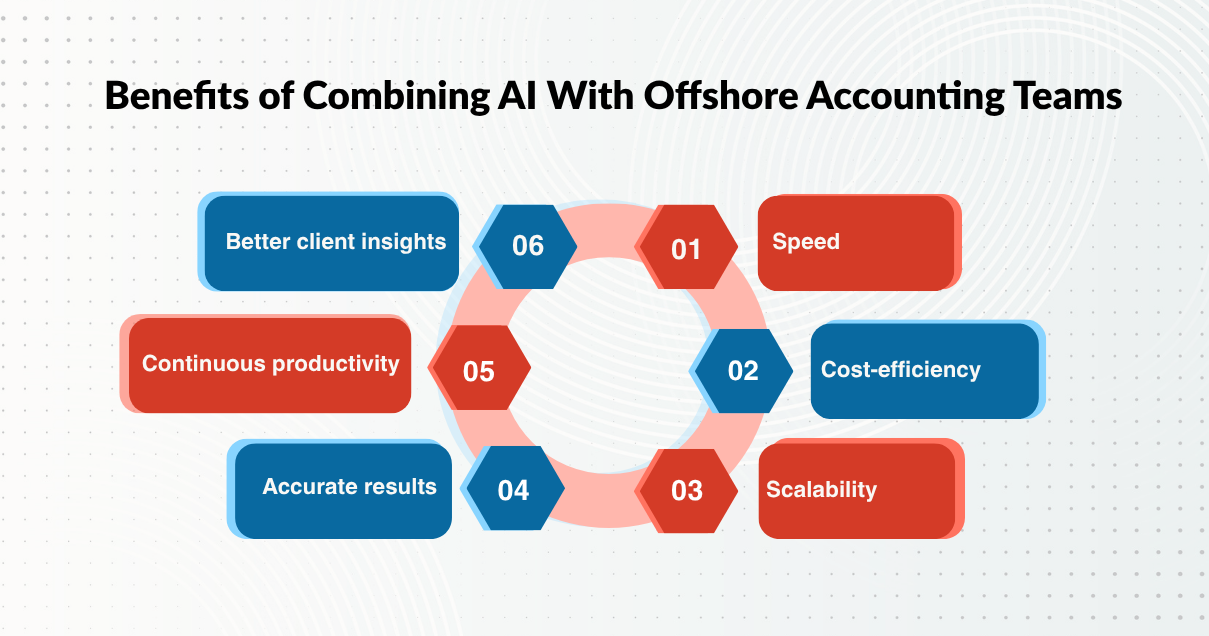

Let’s be direct about the actual outcomes.

Speed: Month-end close that used to take 10 to 15 business days regularly drops to 5 to 7. Tax prep turnarounds improve. Clients notice, and it changes the conversation.

Cost-efficiency: The union of offshore salaries and artificial intelligence leads to cost structures that cannot be beaten at home. Companies will be able to provide reduced prices while increasing their profit margin.

Scalability: Expansion isn’t limited by recruitment. There won’t be a need to panic during peak season. This model scales better than relying only on an in-house team.

Accurate results: AI-powered error detection will find what you could overlook due to rushing through your work. Higher volume of the tasks is always associated with lower errors when done with AI support.

Continuous productivity: Offshore team located in another timezone along with AI software processing your data 24/7 will allow work on the project continuously, including when your in-house team goes to sleep. You enter your office and see a completed project.

Better client insights: When routine work is automated, there’s more capacity for real-time financial dashboards and forward-looking analysis. That’s an upgrade in what the firm actually delivers.

Any honest look at this includes the friction points.

Data security. Client financial data is sensitive. Before engaging any offshore provider using AI tools, understand where data is stored, how it’s protected, and what certifications the provider holds. SOC 2 compliance, encryption standards, and clear data handling policies should be non-negotiable baseline requirements. Don’t take a provider’s word for it. Ask for documentation.

Integration. AI tools work well when properly integrated with existing systems. Poor integration creates new problems. Expect to spend time on setup, and don’t assume it’ll be seamless.

Change management. Staff who are used to doing things a particular way will push back. Getting genuine buy-in means being clear about what’s changing and why, not just announcing it.

Quality oversight. AI makes mistakes. Offshore teams make mistakes. The goal is to catch them before they reach the client. Robust review processes and clear accountability matter just as much as the technology.

Vendor selection. Not every offshore provider that mentions AI has a sophisticated implementation. Some are using basic automation and calling it AI. Ask specific questions about what tools are in use, how they’re configured, and what human oversight sits behind them.

None of these challenges are disqualifying. But walking in without thinking them through is how firms end up with experiences they regret.

A few directions are becoming clear.

Real-time accounting is moving from aspiration to standard. The combination of cloud platforms, AI processing, and offshore delivery is pushing accounting toward continuous close processes where financials are always current. Quarterly reporting cycles are giving way to dashboards that update in near real-time.

Offshore teams are specializing. As AI handles more commodity work, offshore accounting teams are developing deeper expertise in specific areas. US GAAP compliance, R&D tax credits, industry-specific accounting. The generalist offshore bookkeeper is being replaced by something considerably more capable.

Predictive work is becoming accessible. Predictive cash flow modeling and scenario analysis tools are getting easier to use and more accurate. Offshore teams with AI capabilities will be delivering forward-looking analysis, not just historical financials.

Security frameworks are tightening. The regulatory environment around data privacy is getting stricter globally. Offshore providers that invest in compliance infrastructure will have a significant advantage, and firms should be factoring this into provider selection now.

The overall direction of AI in offshore accounting is toward greater capability, tighter integration with client systems, and a delivery model that looks more like a genuine extension of the CPA firm than a separate back-office operation.

Indian Muneem works specifically with CPA firms in the US, UK, Australia, and New Zealand. The client base is practices dealing with real capacity pressure, demanding clients, and a hiring environment that makes growing a domestic team increasingly difficult and expensive.

The model is built around the combination this blog has been describing. AI tools handle data processing, reconciliation, and initial reporting. A team of qualified Chartered Accountants handles review, judgment, and client-facing deliverables. Multiple quality checkpoints sit between the AI-processed work and what reaches the CPA firm.

The team has specific training in the accounting standards and tax frameworks relevant to each market. US GAAP, IFRS, Australian standards, UK tax rules. Offshore bookkeeping services, tax return preparation, payroll processing, financial statement preparation, and management reporting are the core service areas.

Data security is a baseline, not an afterthought. Secure file transfer, access controls, and confidentiality agreements are standard. For firms with specific data handling requirements, the processes exist to accommodate them.

The value is straightforward: more work, done faster and more accurately, at a cost that makes the firm’s numbers work better. The AI-powered model makes it possible. The qualified human team makes it reliable.

AI doesn’t make offshore accounting better by replacing people. It makes it better by giving skilled people the tools to do more, faster, and with fewer errors. The CPA firms getting the most out of this combination are the ones that figured that out early.

The talent shortage isn’t going away. Client expectations aren’t going down. The operational pressure on practices in the US, UK, Australia, and New Zealand is only going to increase. AI in offshore accounting is one of the more practical, proven responses to that pressure available right now.

The firms that act on it now are building a real advantage. The ones that wait will be playing catch-up.

We use cookies and similar technologies to improve your experience, personalise content, and analyse traffic. Some are essential for access to our products and informational resources. Certain services or pages may also be governed by additional Terms of Use. Manage your preferences at any time.