Xero vs QuickBooks: Country-Wise Comparison (2026) – Which Accounting Software Is Right for Your Business?

Table Of Contents

Toggle

The short answer is no. The longer answer is more interesting.

AI is already doing things in accounting that used to take entire teams. It’s reconciling transactions in seconds, flagging anomalies before a human even opens the file, and generating financial summaries that would have taken a junior accountant half a day. So it’s fair to ask: will AI replace accountants, or is this just another wave of automation that reshuffles the deck without flipping the table?

This question is genuinely worth taking seriously, because the answer shapes career decisions, hiring strategies, and how accounting firms position themselves going into the next decade. And the answer isn’t as clean as either side of the debate would have you believe.

Let’s get into it.

The concern makes sense when you look at what’s happened in the last three years. AI tools haven’t just improved, they’ve jumped. What was a novelty in 2022 is now embedded infrastructure in accounting platforms used by real firms every day. Tools like large language models (LLMs), robotic process automation (RPA), and machine learning algorithms aren’t science fiction anymore. They’re in the software your clients are probably already using.

The fear got louder when Goldman Sachs published a 2023 report estimating that around 300 million full-time jobs globally could face some form of automation. Accounting showed up near the top. The media ran with it, and the narrative kind of stuck.

There’s also a cold cost argument underneath all of this. Software subscriptions don’t ask for raises. They don’t call in sick. For a small business owner looking at their bookkeeping bill every month, the appeal of “just let the software handle it” is obvious and real.

But cost and speed aren’t the whole picture, and that’s where the fear starts running ahead of what’s actually happening.

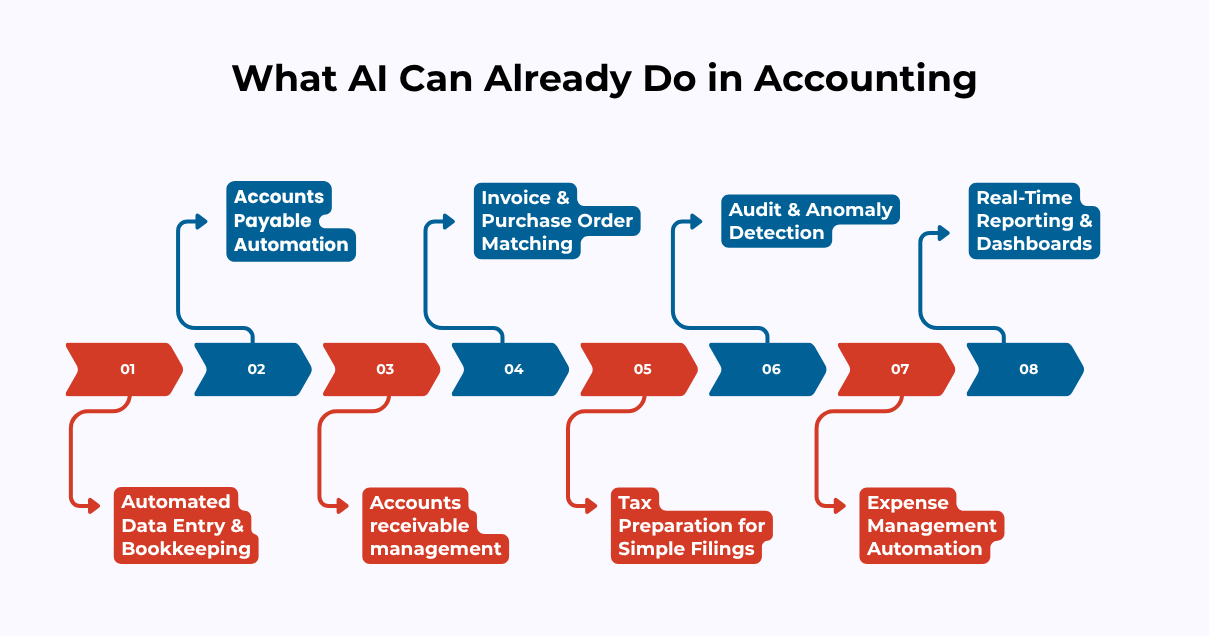

Dismissing AI as overhyped doesn’t help anyone, least of all accountants who need to understand the landscape they’re working in. So let’s be honest about what it actually does well.

Automated data entry and bookkeeping is probably the most mature use case right now. Platforms like Xero, QuickBooks, and Dext can pull from invoices, bank feeds, and receipts, then categorize and record transactions with solid accuracy. What used to take hours now happens in the background.

Accounts payable and receivable has changed a lot too. Matching purchase orders to invoices, catching discrepancies, routing payments, these are tasks that used to need people sitting in front of spreadsheets. Now software handles a lot of it.

Tax preparation for straightforward filings has also moved significantly. Consumer-facing tax software and even the IRS’s Direct File program use AI to identify deductions and generate returns for simple situations. Nothing groundbreaking for complex work, but fast and cheap for the basics.

Where AI genuinely impresses is audit and anomaly detection. Running machine learning models across millions of transactions to flag statistical outliers is something no human team can match on speed. It doesn’t replace the audit, but it makes the audit better.

Expense management platforms, real-time dashboards, automated financial reporting, these are all areas where the technology has matured enough to take real work off people’s plates.

So yes, a meaningful chunk of what accountants used to spend time on is now being done by software. But that doesn’t mean accountants are being replaced. It means their time is being freed up, and the question is what they do with it.

Here’s where a lot of the commentary gets lazy. People either panic about AI taking everything, or they wave it off entirely. Neither is accurate.

The honest reality is that professional judgment is the core of what experienced accountants provide, and that’s not something you can automate. When a client is deciding how to structure an acquisition, whether to go asset deal or stock deal, the answer depends on tax implications, the client’s risk tolerance, seller preferences, jurisdiction-specific rules, and business context that’s been built up over years of working with that client. No AI is making that call.

Client relationships are another thing that just doesn’t translate to software. A CFO navigating a tough year doesn’t want a chatbot. They want someone who knows their business, who’s been through a few of these cycles, who can push back when something doesn’t make sense. That’s worth money in a way that’s hard to quantify but very easy to feel when it’s absent.

Complex tax planning across multiple entities, different jurisdictions, or unusual situations requires strategic thinking that current AI simply doesn’t have. AI can tell you what happened in the numbers. It can’t reliably tell you what to do about it, especially when you’re in territory that doesn’t have a clean precedent.

Forensic accounting is another area where the human factor isn’t optional. Fraud investigations, litigation support, contested valuations, these involve professional testimony, legal accountability, and reasoning that courts and opposing counsel will put under real pressure. Courts don’t accept AI affidavits.

And then there’s ethical decision-making, which gets underestimated in these conversations. Accountants work in situations where what’s legally allowed and what’s professionally right aren’t always the same thing. AI has no values. It has training data and optimization targets. That’s a fundamentally different thing.

This one doesn’t get enough airtime, and it should.

AI hallucination is when a model generates output that sounds correct and confident but is factually wrong. In casual use, this is frustrating. In accounting, it can be genuinely dangerous.

An AI tool summarizing a tax position might cite a deduction limit that changed in legislation it wasn’t trained on. It might apply a depreciation rule incorrectly to a specific asset class. It might produce a financial narrative that contradicts the underlying numbers in a way that’s subtle enough to miss on a quick read.

This isn’t hypothetical risk. Legal professionals have already filed AI-generated briefs citing cases that don’t exist. The accounting equivalent hasn’t made the same headlines, but anyone who thinks it hasn’t happened is being optimistic.

The implication isn’t “don’t use AI.” It’s “never trust AI output without a review from someone who actually understands the work.” Which means the human is still in the loop, and in many cases needs to understand the underlying material well enough to catch what the AI got wrong. You can’t audit output you don’t understand.

AI model accuracy, training data limitations, and clear output verification protocols aren’t optional extras for firms using these tools. They’re baseline requirements.

Being direct about this is more useful than dancing around it.

Data entry clerks and bookkeepers doing routine transaction recording are the most exposed. The work is rule-based and repetitive, which is exactly the kind of work automation handles well. The volume of people needed to do this work is shrinking, and that’s just true.

Payroll processing roles that are purely administrative, running standard calculations each cycle, are in a similar position. Most payroll platforms already do the bulk of this work and have for a while.

Basic accounts payable and receivable clerks in organizations running high transaction volumes will find more and more of their work absorbed by software. Not overnight, but consistently.

Junior tax preparers working on standard returns, W-2 income, straightforward deductions, nothing complex, are competing with consumer software that’s fast, cheap, and accurate enough for simple situations.

The pattern isn’t hard to see. Rule-based, repetitive, structured data. If the task looks the same every time and the rules don’t change much, software can probably do it. This is true across industries, not just accounting.

CFOs and financial controllers live at the intersection of finance and strategy. Their job is to take financial information and connect it to business decisions, communicate with boards, manage through uncertainty, and lead a function through change. AI can surface information for them. It can’t replace what they do with it.

Tax advisors working on complex multi-entity or cross-border situations are doing work that requires deep expertise and professional accountability that software vendors explicitly disclaim. The stakes are high enough that you need a human who’s on the hook.

Forensic accountants, audit partners, and senior auditors are doing work that requires professional standing, testimony, and the kind of judgment that courts and regulators require from an identifiable human being.

Management accountants embedded in businesses as financial partners are becoming more valuable, not less, as AI handles the transactional layer. Their job is increasingly about connecting financial data to business decisions, which requires understanding the business, not just the numbers.

The common factor across all of these is judgment, accountability, or relationships. Those things are durable.

| Capability | AI | Human Accountant |

|---|---|---|

| Processing speed | Extremely fast | Time-limited |

| Routine transaction handling | Excellent | Effective but slower |

| Complex tax planning | Weak | Strong |

| Client communication | Poor | Strong |

| Regulatory interpretation | Risky | Professional standard |

| Catching errors in own output | Limited | Strong |

| Ethical judgment | None | Bound by professional code |

| Handling novel situations | Limited | High |

| Legal accountability | Not applicable | Fully applicable |

| Cost per transaction at volume | Low | Higher |

Neither column makes the other irrelevant. The firms doing this well are figuring out how to combine both, not choose between them.

The better framing isn’t “AI replacing accountants.” It’s AI changing what accountants spend their time on, and that’s a genuinely different thing.

The shift is from data handling toward data interpretation. From running the compliance process toward advising on compliance strategy. From producing the numbers toward explaining what they mean for the business.

Accounting firms leaning into advisory-led accounting right now are finding that AI handles the production work and the accountant focuses on the work that actually differentiates the firm. That’s a better product for the client. It’s also a more interesting job.

But this requires real adaptation. If an accountant’s value proposition is built on doing work that software now does faster and cheaper, the next decade is going to be uncomfortable. If it’s built on judgment, strategy, and client relationships, AI is mostly a productivity tool.

Digital transformation in accounting, cloud-based platforms, and AI-powered financial forecasting tools are all pushing in the same direction. The question is whether accounting professionals are getting ahead of it or waiting to see what happens.

The benefits are real and worth stating plainly.

Speed is the most obvious one. Month-end close processes that used to stretch across two weeks can now get done in two days when AI handles routine reconciliation and reporting. That’s a genuine competitive advantage for any firm that’s managed it well.

Accuracy in high-volume routine work is another genuine win. AI doesn’t get tired at 11 PM before a deadline. For transaction processing at scale, the error rate on AI-handled work is generally lower than on manually-handled work, assuming the underlying data is clean.

Automated bank reconciliation, real-time dashboards, and cloud accounting software give business owners financial visibility they’ve never had before, without waiting for month-end reports. For small and mid-sized businesses especially, that’s a meaningful change in how they can actually run their operations.

Scalability is underrated in this conversation. A growing business can handle significantly higher transaction volumes without proportionally growing its accounting headcount. That structural advantage compounds over time.

This part gets less attention than it deserves.

Garbage in, garbage out. AI tools are only as reliable as the data going into them. A messy chart of accounts, inconsistently formatted invoices, incorrectly set up bank feeds, and the AI will confidently produce wrong answers. Automation amplifies whatever’s already there, good or bad.

There’s a longer-term skills concern that the profession needs to take seriously. If junior accountants never learn the underlying work because AI does it for them, you end up with a generation that can’t verify AI output because they’ve never done the work themselves. You can’t catch errors in something you’ve never learned to do. That’s a real structural problem down the road.

On the liability side, professional responsibility still sits with the human who signed off. AI vendors disclaim liability for errors in their outputs. In most jurisdictions, the accountant who reviewed and approved the work is still professionally and legally accountable. Relying on AI output without proper review isn’t just risky, it may cross professional conduct lines depending on the situation.

Data privacy and security is a growing concern, particularly in the US, UK, Australia, and New Zealand, where regulators are paying closer attention to how sensitive financial data is handled by third-party AI tools. This is not a checkbox issue. It’s a real operational and compliance question for any firm using these platforms with client data.

The profession isn’t heading toward accountants versus AI. It’s heading toward a split between accountants who use AI well and those who don’t.

What’s sometimes called augmented accounting is the direction things are moving: AI handles the transactional and computational layer, and human professionals focus on strategy, interpretation, client relationships, and professional judgment. Done well, this is a better version of the profession. Higher-value work, better client outcomes, and frankly more interesting day-to-day than processing transactions ever was.

The entry-point challenge is real though. The traditional route into accounting through manual bookkeeping and data entry is narrowing, and the profession hasn’t fully sorted out how it trains the next generation when the foundational work is being automated. Continuing professional development, technology literacy, and advisory skills are going to matter more than they used to, and the gap between firms investing in this and those that aren’t is already visible.

AI-driven tax compliance software, integrated accounting platforms, and real-time reporting tools are going to be standard infrastructure within a few years. Firms not already building those capabilities are behind.

Because the stakes are too high and the situations too varied to hand everything over to software.

A business going through a merger needs someone who understands the deal, the client, and the regulatory environment in that specific situation. A founder structuring their business for a future sale needs strategic advice, not a generated report. A business owner facing an audit needs representation, professional judgment, and someone who’s accountable to more than a terms-of-service agreement.

Beyond the complex situations, there’s something simpler: people want to talk to someone. Business owners and CFOs want a person who knows their situation, who will actually pick up the phone, who will push back when something doesn’t add up. That relationship doesn’t come from a chatbot and it doesn’t get replaced by a dashboard.

And in a world where AI output can be wrong in ways that sound completely convincing, having a professional who reviews that output and takes responsibility for it isn’t a nice-to-have. It’s the actual product.

Will AI replace accountants? No. Not in 2026, not in 2030, and not in any foreseeable version of a world where business decisions involve genuine complexity, professional judgment, and legal accountability.

What AI will do, and is already doing, is take over the routine and repetitive parts of the work. That’s going to reshape things significantly. Entry-level roles will change. The skills that matter most will shift. Firms that don’t adapt will feel it.

But the core of what accounting professionals actually provide, judgment, strategy, relationships, and professional accountability, isn’t going anywhere. The accountants who see AI as a tool that lets them work at a higher level will be in a good position. The ones who treat it as a threat to resist, or alternatively as something they can just hand work off to without review, will have a harder time.

The question was never whether to use AI. It’s whether you’re using it in a way that makes you better at your actual job.

We use cookies and similar technologies to improve your experience, personalise content, and analyse traffic. Some are essential for access to our products and informational resources. Certain services or pages may also be governed by additional Terms of Use. Manage your preferences at any time.