Xero vs QuickBooks: Country-Wise Comparison (2026) – Which Accounting Software Is Right for Your Business?

Table Of Contents

Toggle

Here’s something nobody tells you until it’s too late: a clean audit doesn’t mean your money is safe.

Audits check whether numbers are reported correctly. They’re not built to catch someone who’s spent months making sure the numbers look correct while quietly taking the difference. That’s a different problem, and it needs a different kind of professional.

A forensic accounting expert is a professional. Not your external auditor. Not your CFO. Someone trained to pull financial records apart, find where the story breaks down, and build findings solid enough to hold up in court. They sit at the intersection of accounting, investigation, and law. Most financial professionals don’t.

This is worth understanding properly, whether you’ve already got a problem on your hands or you’d rather not.

“Forensic” just means built for legal proceedings. So at the core, a forensic accounting expert is an accountant whose work is designed to survive legal scrutiny. That shapes everything: how they collect evidence, how they document their methods, how they write their reports.

What separates them from a regular accountant isn’t only the investigative angle. It’s the standard they’re held to. Their findings need to be reproducible. Their methodology has to be explainable to someone with no financial background. And they need to defend every conclusion under cross-examination. That’s a completely different bar than preparing a set of accounts.

In practice, they investigate suspected fraud inside companies, support commercial litigation, work on business valuation disputes, assist with contested insurance claims, and help businesses under regulatory review understand their own exposure. Some specialize in anti-money laundering (AML) compliance and tracing funds through layered corporate structures.

Many work within dedicated forensic accounting firms built around nothing but this. Others sit within broader chartered accountancy practices with a specialist forensic arm. Either way, what you’re paying for is the investigative mindset combined with legal rigor. That combination is genuinely rare.

It depends on the case. That’s an honest answer, not a deflection.

On the fraud side, the work is about following transactions where they don’t want to be followed. Employee embezzlement rarely looks like embezzlement in the books. It looks like legitimate expenses, vendor payments, payroll entries. The forensic accountant finds the pattern underneath the appearance. They run journal entry testing to spot unusual approvals or timing. They cross-reference vendor records against employee details. They use Benford’s Law analysis to check whether numbers follow the statistical distribution you’d expect from real figures, because manufactured numbers often don’t. They’re not reading the books. They’re reading through them.

On the litigation side, it looks different. If two companies are in a dispute and one is claiming lost profits, someone has to calculate what those profits actually were, using methodology that holds up in court. That’s the forensic accounting expert’s job. They build the model, document the assumptions, produce a report a judge can actually use. And if the other side challenges the numbers, they sit in the witness stand and defend them. Expert witness testimony is a core part of this work, and it’s one of the clearest things that separates forensic accountants from financial consultants.

Business valuation disputes come up constantly in partnership dissolutions, shareholder buyouts, and divorce proceedings involving business assets. When one side says the business is worth $4 million and the other says $1.2 million, someone’s assumptions are wrong or the numbers have been shaped. A forensic accounting expert goes through the methodology and the underlying data and gives an independent opinion on where the gap actually comes from.

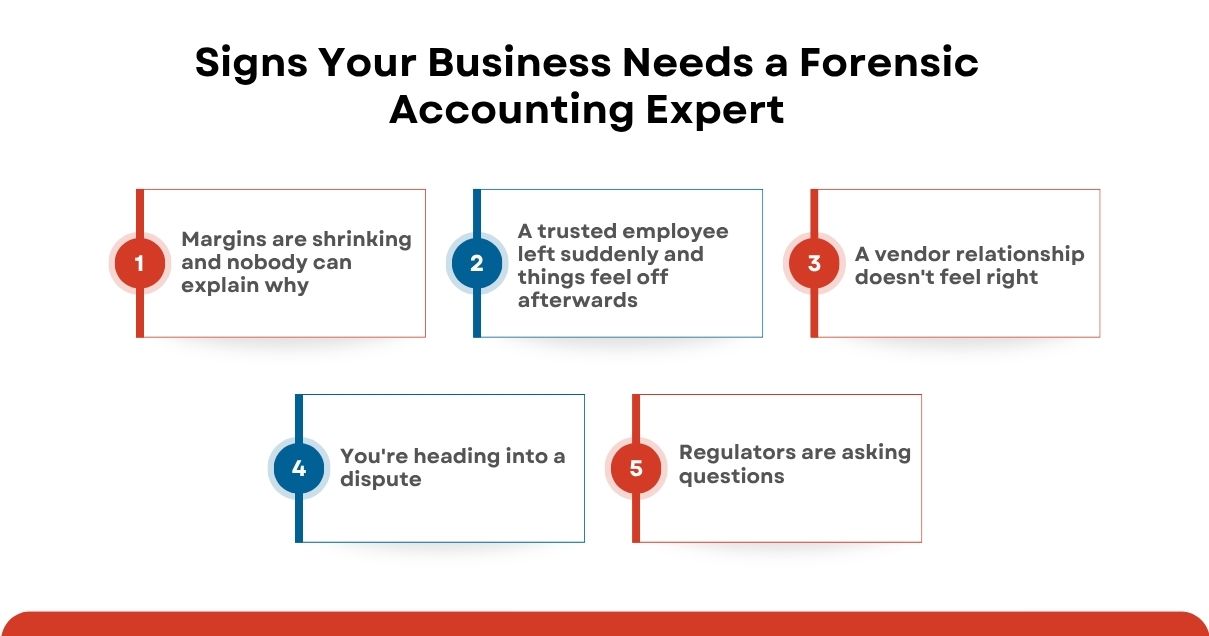

Here are the situations that actually bring businesses to a forensic accountant’s door.

| Traditional Accountant | Forensic Accounting Expert | |

| Primary goal | Accuracy and compliance | Investigate what’s actually going on |

| Starting assumption | Let’s verify this is correct | Let’s find out if it is |

| Approach | Sampling, testing controls, reviewing documentation | Transaction-level review, tracing, interviews, document authentication |

| What they’re looking for | Errors and material misstatements | Patterns, anomalies, things that don’t fit |

| Can they catch deliberate fraud? | Not reliably. Sophisticated fraud is built to pass audits | Yes. That’s the whole job |

| Output | Financial statements, audit opinions | Investigation reports, damage calculations, expert testimony |

| Legal standing | Not typically used in court | Built for court, regulators, and insurance adjusters |

| Who they report to | Management, shareholders | Lawyers, boards, courts, regulators |

It starts with a careful conversation about what’s known and what’s suspected. The forensic accounting expert will define a scope with you: which entities, which time periods, which transaction types. A clear scope keeps the investigation focused and defensible.

Evidence preservation comes before analysis. If the matter ever becomes litigation, the chain of custody for records and data will be scrutinized. Financial records, emails, system exports, approval histories all need to be secured in a way that proves they haven’t been touched after collection.

Then the analysis. Cash flow tracing to follow funds from source to destination. Accounts payable review to identify vendor patterns that don’t match real business activity. Payroll reconciliation. Bank statement matching against the general ledger. The specific procedures depend on the suspected issue, but the common thread is depth. Not samples. Line by line.

Interviews happen once the documentary work has surfaced enough to know which conversations matter. These aren’t casual. They’re conducted carefully, because anything said here could matter later.

The output is a report: what was found, how it was found, and what it means financially. For litigation matters, this extends to testimony. The forensic accounting expert defends every number and every methodology decision across from opposing counsel. That’s why the work is documented so carefully from day one. It’s built to be tested.

Timelines depend on scope. A focused review might be done in a few weeks. A complex cross-border investigation can run six months or more. What drives the timeline isn’t the firm’s pace. It’s the volume of data, the availability of records, and whether the relevant parties are cooperating.

Indian Muneem Chartered Accountant works with businesses across the US, UK, Australia, and New Zealand on forensic matters ranging from internal fraud reviews to full commercial litigation support. The investigative depth is there for complex cases. So is the communication clarity that makes findings actually useful to lawyers, boards, and courts.

For clients who already work with Indian Muneem on broader accounting, there’s a real advantage: no onboarding period. The team already knows the business structure, the financials, and the relationships. When a fraud issue or dispute comes up, the forensic work can start properly from day one. That familiarity cuts both time and cost.

What matters most to clients isn’t just technical competence. It’s having a forensic accounting expert who explains what’s happening at every stage in plain terms, not just in the final report. Fraud and financial disputes are already stressful enough. Clarity throughout makes a real difference.

If your numbers don’t add up and you need someone who can figure out why, reach out to Indian Muneem. That’s exactly what we do.

We use cookies and similar technologies to improve your experience, personalise content, and analyse traffic. Some are essential for access to our products and informational resources. Certain services or pages may also be governed by additional Terms of Use. Manage your preferences at any time.