Xero vs QuickBooks: Country-Wise Comparison (2026) – Which Accounting Software Is Right for Your Business?

Table Of Contents

Toggle

Most businesses buying, selling, or holding crypto are doing their accounting wrong. Not because they’re careless. Because crypto genuinely breaks traditional accounting systems, and a lot of firms are still trying to force-fit a square peg into a round hole.

Cryptocurrency accounting services exist precisely because of this gap. Crypto doesn’t behave like cash or stocks. It has its own valuation problems, its own tax rules, and its own reporting requirements that shift depending on which country you’re operating in.

If you’re running a business in the US, UK, Australia, or New Zealand and dealing with digital assets in any form, you need a proper accounting framework built for how crypto actually works. This guide covers everything you need to know to get that right.

Essentially, cryptocurrency accounting services involve accounting and consulting services that manage the entire financial life cycle of digital currencies. It entails tracking every transaction, determining cost basis, selecting proper valuation methodologies, ensuring accurate tax returns, and ensuring that your financial books are compliant with reporting standards in your country.

Where this gets interesting is in the scope. A solid crypto accounting service doesn’t just log entries. It deals with:

Crypto-to-fiat conversions and the gains or losses they trigger. DeFi transactions like liquidity provision, yield farming, and staking rewards each have different tax treatment. NFT sales and how to classify them. Airdrops and hard forks are treated inconsistently across countries by regulators. Cross-border crypto payments, where you might have obligations in more than one jurisdiction.

It’s a wide field. And the more active your crypto operations, the more complex the accounting gets.

Let’s be direct. Crypto accounting is genuinely hard. This isn’t just professionals being precious about their expertise.

The blockchain transaction volume most businesses generate is enormous. Even a mid-sized operation accepting crypto payments can rack up thousands of transactions a month. Each one needs to be matched, valued at the point of receipt, and tracked for future capital gains or ordinary income classification.

Then there’s the issue of multiple wallets and exchanges. Businesses rarely keep everything in one place. You might have funds on Coinbase, Binance, a hardware wallet, and a DeFi protocol simultaneously. Reconciling all of that manually is not realistic.

DeFi protocol complexity has also escalated sharply. When you provide liquidity to a pool, you often receive LP tokens in return. Are those taxable at receipt? What happens when you withdraw and the ratio of assets has changed? What about impermanent loss? Most mainstream accounting frameworks don’t have clear answers yet.

Stablecoin transactions add another layer. Many businesses assume swapping USDC for USDT is tax-neutral. In some jurisdictions, it isn’t. It can be treated as a disposal.

On top of all this, regulatory reporting requirements have gotten stricter. The IRS, HMRC, the ATO, and Inland Revenue in New Zealand have all ramped up enforcement and guidance. Staying compliant isn’t optional. It’s just a question of whether you do it right or scramble at year-end.

Also Read: What Are End-to-End Bookkeeping Services: Complete Financial Support for Growing Businesses

Regulations aren’t uniform. Here’s what businesses need to know across the main English-speaking markets.

United States: The IRS considers cryptocurrency as property. This means that every transaction is considered a taxable event, and trading one cryptocurrency for another is no exception. Short-term capital gains, or assets that have been held for less than a year, are considered ordinary income. Long-term capital gains are taxed at reduced rates. Additionally, businesses must track FIFO, LIFO, or identify the specific method and use it consistently. The creation of Form 1099-DA in 2025 requires brokers to report transactions to the IRS, making the consequences of incorrect cryptocurrency tax reporting much more severe.

United Kingdom: HMRC treats crypto as a capital asset. Businesses face Capital Gains Tax on disposal and Income Tax on mining rewards, staking income, and airdrops treated as income. The UK also uses a specific pooling method for calculating gains, which is different from what most US-based software defaults to. Getting this wrong is common.

Australia: The ATO has been proactive. Crypto received as payment for goods or services is treated as assessable income. Capital gains apply on disposal. Australia uses a cost base system and allows a 50% CGT discount for assets held more than 12 months, but that’s for individuals. Business entities have different rules. The ATO has also confirmed that DeFi transactions can be taxable events depending on whether you’re genuinely transferring ownership.

New Zealand: Inland Revenue treats crypto as property for tax purposes. There’s no capital gains tax in NZ, but if you’re trading with the intention to profit, those gains are taxable as income. This “intention test” is fact-specific and has tripped up a lot of businesses. GST implications for crypto transactions in New Zealand are also still evolving.

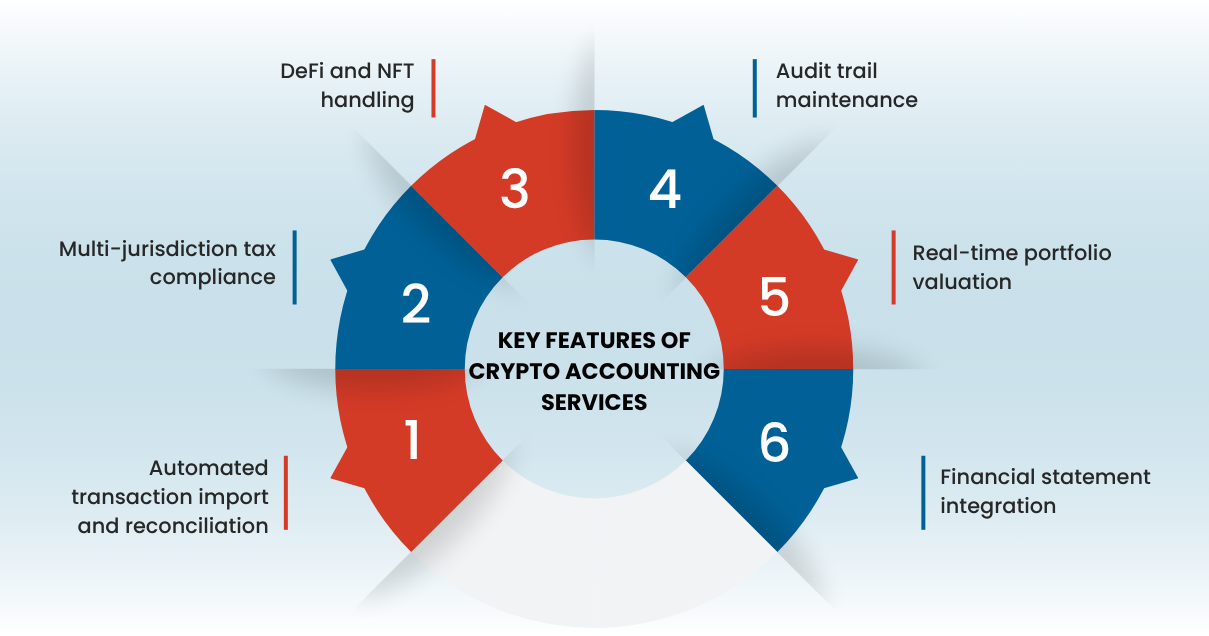

Not every firm offering crypto accounting is actually equipped to handle it. The real differentiators are worth knowing.

Automated transaction import and reconciliation is non-negotiable. Any professional service should be pulling data directly from exchanges and wallets via API, not relying on you to export CSVs manually.

Multi-jurisdiction tax compliance matters if your business operates across borders or if you have clients, contractors, or suppliers in different countries.

DeFi and NFT handling separates the specialists from the generalists. If a firm can’t clearly explain how they’d treat your yield farming income or your NFT royalties, that’s a gap.

Audit trail maintenance is critical. Every transaction should have a clear record of when it occurred, what the value was at that point, and how it was classified. This is what protects you if you’re ever queried by a tax authority.

Real-time portfolio valuation and financial statement integration round out a full-service offering. Your crypto holdings need to show up correctly in your balance sheet, and the method for valuing them matters for how your business looks to investors and lenders.

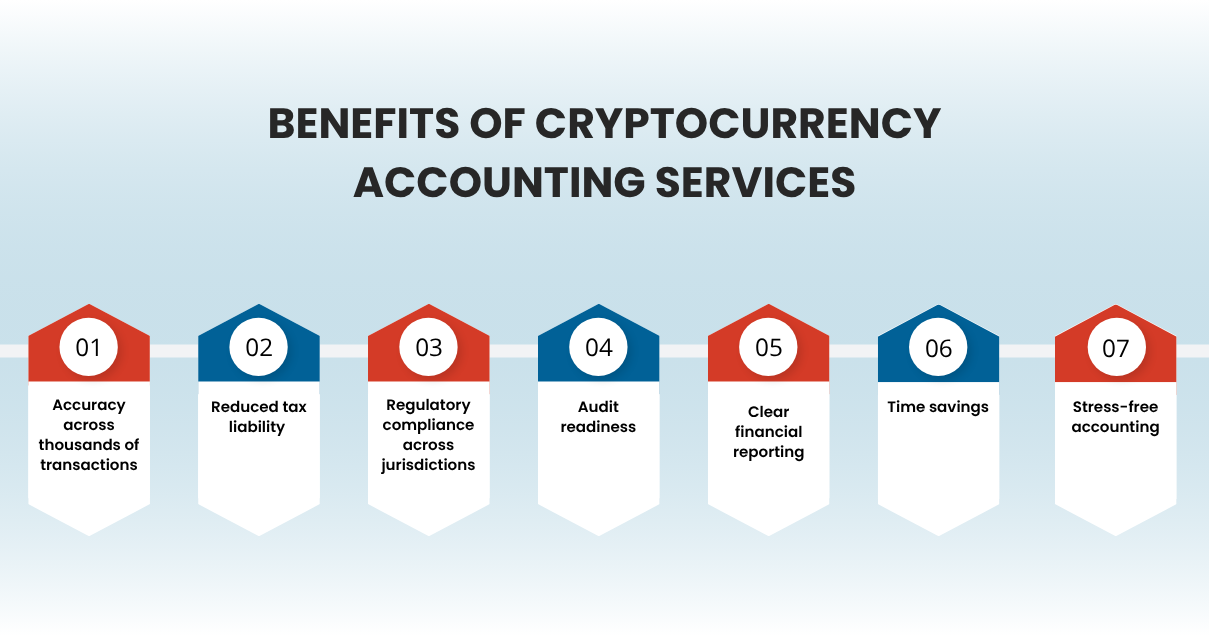

1. Accuracy across thousands of transactions: Manual tracking fails at scale. Professional services handle volume without compromising accuracy.

2. Reduced tax liability through smart planning: Professionals identify legal strategies like tax-loss harvesting and optimal cost basis methods that businesses miss when doing it themselves.

6. Time savings: Your team should be running your business, not manually matching wallet addresses to transaction IDs.

7. Peace of mind: Crypto taxation is genuinely complicated. Knowing it’s handled correctly removes a real source of business risk.

Even experienced finance teams run into specific problems with crypto. Here are the ones that come up most often.

Valuation at the point of transaction: Crypto prices move fast. Recording the correct fair market value at the exact moment of a transaction requires reliable data sources and automated systems.

Missing historical data: Businesses that have been holding crypto since 2020 or 2021 often have patchy records. Reconstructing transaction history from blockchain data is possible but time-consuming.

Interoperability between accounting software and crypto platforms: Not every exchange plays nicely with accounting systems. Data gaps and formatting issues create reconciliation headaches.

Classification errors: Is a staking reward ordinary income or a capital receipt? Is a token received in a partnership deal an expense or a loan? These classification decisions have real tax consequences.

Staff knowledge gaps: Traditional accountants who haven’t specialized in crypto often make conservative but incorrect assumptions that either create unnecessary tax liability or compliance risk.

The toolset in this space has matured significantly. Professionals working in crypto accounting typically use a combination of the following.

Koinly, CoinTracker, and TaxBit are the main dedicated crypto tax platforms. Each has strengths depending on jurisdiction and the types of transactions involved. TaxBit, for example, has strong integrations for US tax reporting. Koinly is widely used across the UK, Australia, and New Zealand.

Xero and QuickBooks still act as the backbone for general ledger and financial reporting. The problem is that native crypto support for Xero and QuickBooks is limited, and the process often involves taking data from a crypto-specific tool after it’s been reconciled and sending it to the general accounting software.

Chainalysis and other blockchain analysis software are often utilized if a business requires forensic-level transaction analysis, which is often required for industries with high compliance needs or large transaction volumes.

API integrations with large exchanges like Coinbase, Binance, Kraken, and wallets can help reduce manual data pulls, greatly decreasing errors.

E-commerce businesses accepting crypto payments need proper income recognition and FX gain tracking. Tech startups that raised capital in tokens need to account for that fundraising correctly. Investment firms and family offices holding digital assets as part of a portfolio need accurate valuations and tax reporting. Mining operations have their own specific income recognition rules. Web3 companies and DAOs often have entirely crypto-denominated operations that require a different accounting lens.

Even traditional businesses paying contractors or employees in crypto need proper records. That’s a deductible expense in most jurisdictions, but only if it’s documented correctly.

A few practical things to assess before signing on with any firm.

First, check their actual experience with crypto, not just that they’ve “done some crypto work.” Ask specifically how they handle DeFi transactions, staking income, and multi-wallet reconciliation. If the answers are vague, that tells you something.

Second, check their jurisdiction expertise. A firm that’s excellent with US crypto taxes might not understand the pooling method the UK uses or the intention test in New Zealand. You need someone who knows your specific regulatory environment.

Third, look at their tooling. Are they using purpose-built crypto accounting software or trying to do everything manually in a spreadsheet? Scale and accuracy require proper tools.

Fourth, ask about their audit support process. If you ever receive a query from a tax authority, how does the firm respond? Do they hold your records in a way that makes audit response straightforward?

Finally, understand their pricing model. Crypto accounting fees often scale with transaction volume. Get clarity on what’s included and what triggers additional costs.

The trajectory is clear. Regulatory frameworks are tightening globally. The OECD’s Crypto-Asset Reporting Framework (CARF) is being adopted by more countries and will significantly increase automatic information exchange between tax authorities. Businesses with any meaningful crypto exposure will face more scrutiny, not less.

At the same time, the technology is improving. Better API integrations, smarter reconciliation tools, and more robust blockchain data analytics mean that the accounting process itself will become more automated. But automation needs oversight. The rules are still evolving, and human judgment on how to classify novel transaction types remains essential.

Tokenized real-world assets and the intersection of traditional finance and DeFi are also creating new accounting questions that regulators haven’t fully answered yet. Businesses that build proper accounting infrastructure now will be better positioned as those rules emerge.

Crypto accounting is not a niche problem anymore. It’s a mainstream business challenge for any company with meaningful digital asset exposure. And the cost of getting it wrong, whether that’s underpaying tax, overpaying due to poor planning, or failing an audit, is real and growing.

Cryptocurrency accounting services done properly protect your business, reduce your tax burden legally, and give you clean financial data you can actually use to make decisions.

IMCA brings specialist expertise in cryptocurrency accounting services for businesses in the US, UK, Australia, and New Zealand. From multi-wallet reconciliation to multi-jurisdiction tax compliance, DeFi transaction handling, and full financial statement integration, IMCA has the tools, the knowledge, and the hands-on experience to manage your crypto accounting with accuracy and confidence.

Whether you’re just starting to accept crypto payments or you’re running a full Web3 operation, IMCA can handle it.

Get in touch with IMCA today and take crypto accounting off your plate, for good.

It's basically keeping proper track of all your crypto activity, buying, selling, swapping, and earning, so your books are accurate and you're not scrambling when tax time hits.

Tax authorities don't see crypto as "invisible money." The IRS, HMRC, ATO, they all want their cut. No records means no defense if they come knocking.

Most professionals connect exchanges and wallets via API to tools like Koinly or TaxBit. It pulls everything automatically, values it correctly, and feeds into your main accounting software.

Depends where you are. The US and Australia tax it as property. UK charges CGT on disposals. New Zealand taxes profits if you're trading with intent. Staking and DeFi income? That's a whole separate conversation.

For the general ledger, sure. But Xero or QuickBooks alone won't cut it. You still need a crypto-specific tool handling the valuations and reconciliation before that data flows through.

Date, amount, value in local currency at the time, transaction type, wallet addresses, and fees. Keep everything for at least 5 to 7 years. Yes, even the small stuff.

US follows IRS Notice 2014-21. UK goes by HMRC's Cryptoassets Manual. Australia uses ATO guidance. New Zealand follows Inland Revenue's property income rules. OECD's CARF is also worth watching if you operate across borders.

Koinly, TaxBit, or CoinTracker for the crypto side. Xero or QuickBooks for your general ledger. Chainalysis if you need deeper on-chain tracing. Exchange APIs to avoid manual data entry altogether.

Use the fair market value at the exact time of each transaction, pulled from a major exchange. For your balance sheet, it depends on local standards, some use historical cost, others use current market value.

If you're beyond a few transactions a year, honestly yes. Cost basis tracking, DeFi classification, multi-country compliance, it adds up fast. Getting it wrong costs more than the accountant ever would.

We use cookies and similar technologies to improve your experience, personalise content, and analyse traffic. Some are essential for access to our products and informational resources. Certain services or pages may also be governed by additional Terms of Use. Manage your preferences at any time.