Xero vs QuickBooks: Country-Wise Comparison (2026) – Which Accounting Software Is Right for Your Business?

Table Of Contents

Toggle

Most farm businesses bleed money not from bad harvests but from bad records. Prices shift, seasons change, and costs pile up quietly until a farmer looks up one day and can’t tell if last year was profitable or not. That’s not a farming problem. That’s an accounting problem and exactly why Farm Accounting made easy matters.

This farm accounting guide is written for farm operators and agribusiness managers who know their land but want to know their numbers just as well. We’ll cover what farm accounting actually involves, why it’s different from regular business accounting, how farm bookkeeping works day-to-day, and how an agriculture chart of accounts fits into all of it.

Let’s get into it.

Farm accounting is the process of tracking, recording, and reporting the financial activity of an agricultural operation: income from crops and livestock, expenses like feed and fertiliser, assets like equipment and land, and liabilities like operating loans.

Here’s the thing, though: farm focused accounting isn’t just regular business accounting with a paddock in the background. Agriculture has financial quirks that most generic accounting systems simply aren’t built for.

Biological assets, for one. Crops in the ground and livestock are living assets that change in value as they grow. Under IAS 41 (Agriculture) (which New Zealand follows through its adoption of NZ IFRS), these need to be reported at fair value rather than just cost. That’s a fundamentally different treatment from how most businesses handle inventory.

Then there’s cash flow timing. A dairy farm might pull in the bulk of its revenue during the spring flush and early summer, then run relatively lean through winter. That pattern looks terrible on a standard cash flow statement unless you understand how agricultural cycles work. Lenders who don’t understand this have declined perfectly healthy farms.

Commodity price risk is another one. For New Zealand farmers specifically, Fonterra payout fluctuations alone can swing a dairy operation’s profitability by hundreds of thousands of dollars in a single season, and that’s before you factor in shifts in global lamb and beef prices. Managing that exposure shows up in the financials in ways you simply won’t see in most other industries.

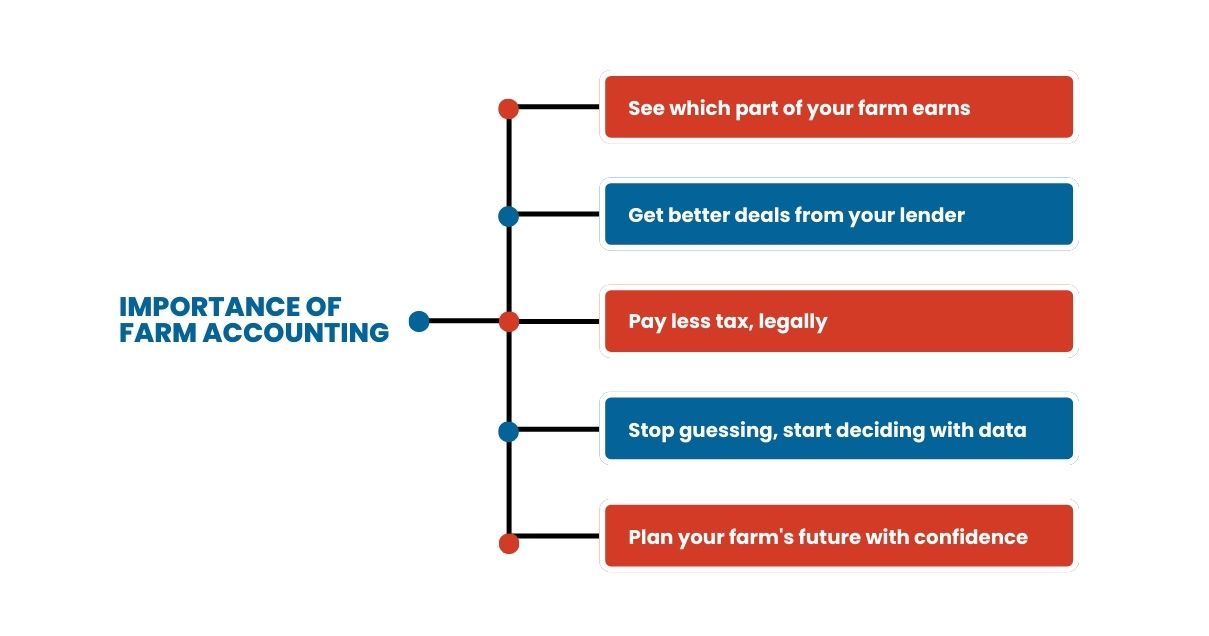

Running a farm on bank balance visibility alone is genuinely risky. You could be making money on paper and still run out of cash before the next payout. You could be losing money on one enterprise while another one masks it. You’d never know.

New Zealand farms commonly run multiple enterprises: dairy, sheep and beef, cropping, or combinations of all three. Without proper accounting, there’s no way to tell which enterprise is carrying the operation and which one is dragging it down. Enterprise budgeting inside your accounting system lets you see gross margins per enterprise, per hectare, or per animal. That’s where the real insight lives.

Rural lenders like Rabobank, BNZ Rural, ANZ Agri, and FMG have seen every kind of farm financials. They can spot messy records immediately, and messy records cost you in the form of higher margins or declined applications. A clean farm balance sheet that properly reflects land value, equipment depreciation, and loan positions puts you in a completely different negotiating position.

New Zealand farm tax has its own landscape. Livestock valuation method elections (national standard cost, herd scheme, or market value) each carry different implications and you can’t revisit them casually. GST on farm supplies and sales, depreciation under IR rules, provisional tax planning for lumpy farm income. None of this manages itself. The farmers who consistently pay less tax aren’t luckier; they have better records and better advisors.

Should you take on that extra 50 hectares? Is your machinery cost per hectare trending up? Is your cost of production for milk solids sitting comfortably below your Fonterra farmgate milk price, or are you closer to break-even than you think? These questions don’t have gut-feel answers. They have accounting answers.

Farm succession is complicated, arguably more complicated in New Zealand than almost anywhere, given land values and family dynamics. Getting accurate land and asset valuations into your records well before any transition planning begins is not optional. By the time you need those numbers, it’s too late to start building them.

Bookkeeping is the unglamorous part of farm accounting, and also the part that determines whether everything else is useful or not. Without accurate, consistent transaction recording, your financial statements are just estimates dressed up in formatting.

Farm bookkeeping is the ongoing work of capturing every financial transaction as it happens. What the bank received. What was paid to the stock firm. What the fuel bill came to. It’s the raw data layer. Everything else sits on top of it: reports, tax returns, loan applications, management decisions.

Farm income is messier than it looks. A New Zealand farming operation might draw from all of the following in a single year:

Each of those streams gets different tax treatment and feeds into different enterprise profitability calculations. Throwing them all into one “farm income” account makes your records useless for any purpose beyond the most basic tax filing.

The expense side is where most farm bookkeeping either earns its keep or wastes everyone’s time. Tracking expenses in broad buckets like “operating costs” or “farm supplies” means you can file a tax return but can’t answer almost any useful management question.

What you actually need is granular tracking across:

Once you know your all-in cost of producing a kilogram of milk solids or a kilogram of lamb, marketing decisions become much less stressful. You know your floor.

Many farms run on cash basis bookkeeping through the year, recording income when cash arrives and expenses when they’re paid. Fine. Simple. Gets the job done week to week.

But cash basis alone gives you a distorted picture of profitability because it ignores what you own and what you owe at any given point. At year-end, you need accrual adjustments to get to a true result:

That adjustment process is what turns a basic cash ledger into a set of financial statements you can actually use.

The basic structure covers five areas:

Every single transaction you record gets assigned to one of those buckets. That’s the whole system in principle.

On most New Zealand farms, the expense categories get the most attention, and rightly so. Splitting costs into meaningful accounts rather than catch-all categories is what makes cost of production analysis per kilogram of milk solids, per stock unit, or per hectare actually possible. That’s the number that tells you whether you’re genuinely profitable or just cash-flow positive by luck of timing.

You don’t need a large or complex system to start. Even 25 to 30 well-chosen accounts gives a small-to-medium farm a workable financial picture. Add accounts as your operation grows or as you take on new enterprises.

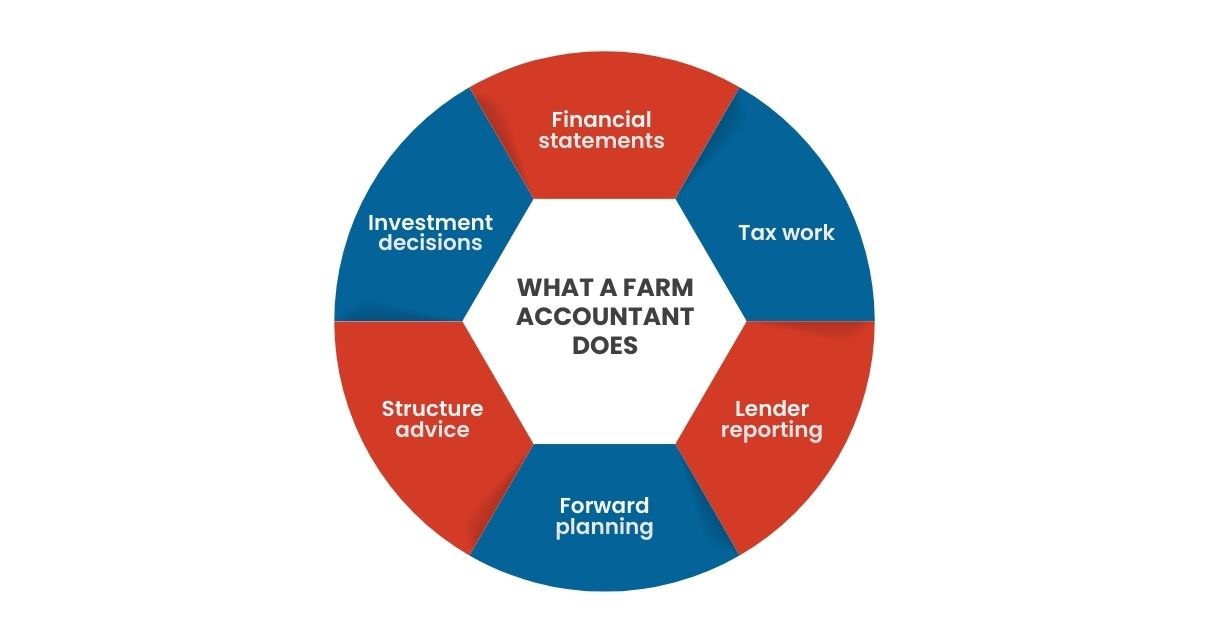

A farm accountant who only surfaces at tax time is not really a farm accountant. They’re a tax agent. In a well-run operation, a proper agricultural accountant is involved throughout the year and across several different functions.

Financial statements: producing monthly or quarterly farm income statements, balance sheets, and cash flow statements. For farms that need to comply with formal reporting standards, this means working within Farm Financial Standards Council (FFSC) guidelines, which set the benchmark for how agricultural financial statements should be structured.

Tax work: New Zealand farm tax is specific. IR3 filing for self-employed farmers, livestock valuation method elections, provisional tax timing, and GST return accuracy across farm inputs and outputs. Done well, this isn’t just compliance. It’s planning that actively reduces what you pay.

The best farm accountants sit somewhere between financial advisor, tax specialist, and business partner. The ones who understand agricultural economics, not just accounting standards, are worth considerably more than their fee.

If your current farm accounting system is a folder of receipts and a bank statement, here’s a practical path forward:

This farm accounting guide covers the framework, but frameworks only do something when they’re used consistently. Whether you manage finances on your own or partner with professional farm accounting services, the numbers will benefit you once you take a closer look at them.

Agriculture is one of the most capital-intensive, risk-heavy businesses around. The farms that manage that risk well don’t just know their land. They know their numbers.

Indian Muneem Chartered Accountant helps agribusinesses and farm operations manage their financial records with clarity and accuracy. Reach out to learn how we can support your farm’s accounting needs.

Follow Us:

We use cookies and similar technologies to improve your experience, personalise content, and analyse traffic. Some are essential for access to our products and informational resources. Certain services or pages may also be governed by additional Terms of Use. Manage your preferences at any time.