Year-End Accounting for New Zealand Businesses: A Practical Guide

The end of the financial year in New Zealand is on 31st March. And if you are one of those people who finds themselves scrambling around on the 28th trying to find receipts, reconcile accounts, and work out what happened to that supplier invoice from August, then you are not alone. But there’s a better way. A solid checklist for year-end accounting in New Zealand doesn’t just save you time. It saves you money, keeps IRD off your back, and gives you a clear picture of where your business actually stands.

Now, look at each of your bank accounts, credit cards, and loan accounts. Are there any discrepancies that you haven’t accounted for? Get them sorted out now. These are often due to double-counted transactions, missing invoices, or bank fees that were incorrectly assigned. If you don’t get them sorted out, they’ll add up, and your financial reports will be telling you a different story altogether.

Also, take stock of your accounts receivable and accounts payable. Who owes you money? Who do you still owe? Aged receivables, like invoices that are 90+ days overdue, may need to be written off as bad debts. This is actually a deductible expense in NZ, so don’t ignore it.

GST compliance is non-negotiable in New Zealand. At year-end, you need to make sure every GST return you’ve filed during the year is accurate and reconciles to your accounting records. If your numbers don’t match what’s in your books, that’s a red flag for you and for Inland Revenue.

Check that input tax credits have been claimed only on legitimate business expenses. Personal expenses that accidentally got coded as business ones are a common audit trigger. If you use your vehicle for both personal and business purposes, make sure you’ve got a logbook or are using an approved IRD method for the split.

For businesses on an invoice basis (rather than payments basis), review any invoices issued near year-end that haven’t been paid yet. These still count as income in the year they were invoiced, not when the cash arrives. This catches a lot of people out.

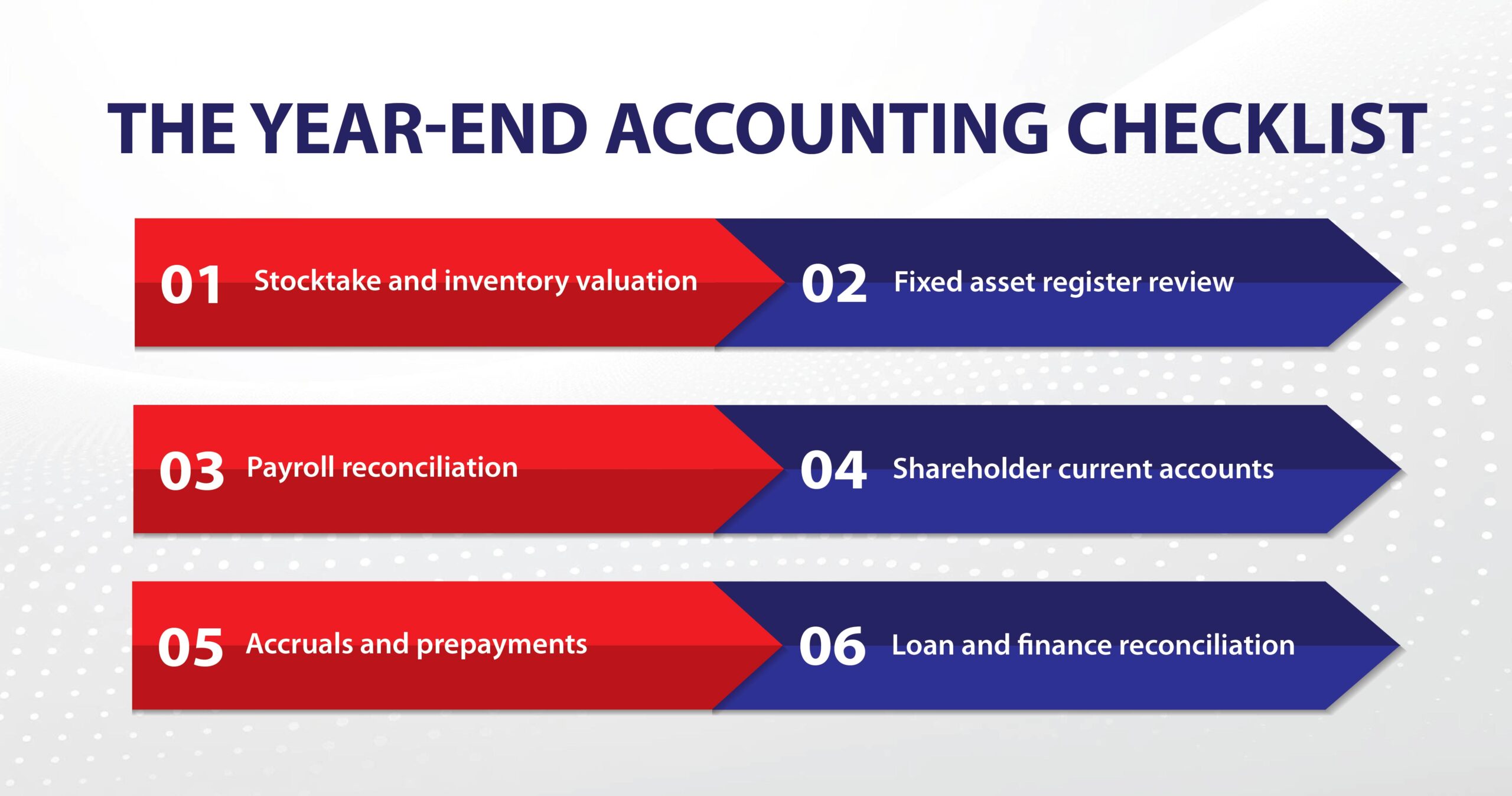

If you carry inventory, you need a physical count as of 31 March. NZ tax rules require inventory valuation at cost or market value, whichever is lower. Don’t just trust your software, count it. Discrepancies between your physical count and system records need to be investigated and adjusted.

If you have employees, reconcile your total PAYE paid to IRD against your payroll records. The introduction of payday filing in NZ means errors surface faster now, but year-end is still the time to catch any gaps. Also confirm that employee KiwiSaver deductions and employer contributions are correct and have all been filed and paid.

For companies, shareholder current accounts need careful review. If a shareholder has drawn more from the company than they’re entitled to, this can create an overdrawn current account, which has fringe benefit tax (FBT) or interest implications under IRD rules. Don’t leave this one for your accountant to find at the last minute.

You need to accrue or prepay expenses that have been incurred but not yet invoiced. This is important so that your profit and loss account reflects the correct period. For example, wages earned in the last week of March but paid in April, or insurance premiums paid for the next year.

If your company pays director fees, these need to be declared and have the correct PAYE deducted. Sometimes this is left until the end of the year as a journal entry. If that’s the case, make sure it’s processed before 31 March, not after.

Also, review whether you need to make a provisional tax payment. If your residual income tax (RIT) last year was over $5,000, you’re in the provisional tax regime. Underestimating or not paying the provisional tax can result in use-of-money interest from IRD. Run an estimate before year-end so you’re not blindsided.

Once the reconciliation and adjustments are done, you’ll be generating your annual financial statements, the balance sheet, the profit and loss, and often a cash flow statement. A lot of business owners sign off on these without really reading them. That’s a missed opportunity.

Not claiming all allowable deductions is also surprisingly common. Home office expenses, vehicle costs, professional subscriptions, training, and development. These are all legitimate deductions for many NZ businesses. If your accountant doesn’t ask about them, you need to bring them up.

And if you need support from an experienced team that genuinely understands New Zealand’s compliance landscape, that’s what Indian Muneem Chartered Accountant is here for.

Follow Us: