Xero vs QuickBooks: Country-Wise Comparison (2026) – Which Accounting Software Is Right for Your Business?

Table Of Contents

Toggle

Most businesses don’t fail because the product was bad or the team was weak. They fail because the money ran out before anyone saw it coming. That’s not bad luck. That’s bad planning. And it’s exactly why the budgeting and forecasting consulting services market has been getting serious attention from business owners, CFOs, and investors over the past few years.

The market isn’t new. But what’s happening inside it right now is. The tools have changed, the expectations from lenders and investors have gone up considerably, and the old habit of dusting off last year’s budget, bumping the numbers by five percent, and calling it done? That approach is starting to cost people real money.

If you run a business in the US, UK, Australia, or New Zealand, and you’re still treating financial planning as a once-a-year box-tick, this is worth reading. Not because it’s alarming, but because the businesses pulling ahead of their peers right now are doing something different with their financial planning, and it’s worth understanding what that looks like.

Put simply, it is a part of the professional services industry where firms and advisors help businesses get a proper handle on their financial future. Not just the annual budget, but the whole function: rolling forecasts, cash flow management, variance analysis, scenario modeling, and the kind of long-range financial planning that actually connects to how the business operates day to day.

It’s a broad space. On one end, you’ve got large consulting firms helping enterprise clients build entire financial planning and analysis (FP&A) functions from scratch. On the other, you’ve got chartered accountants and boutique advisors helping growing mid-sized businesses replace their chaotic spreadsheet process with something that gives them real visibility.

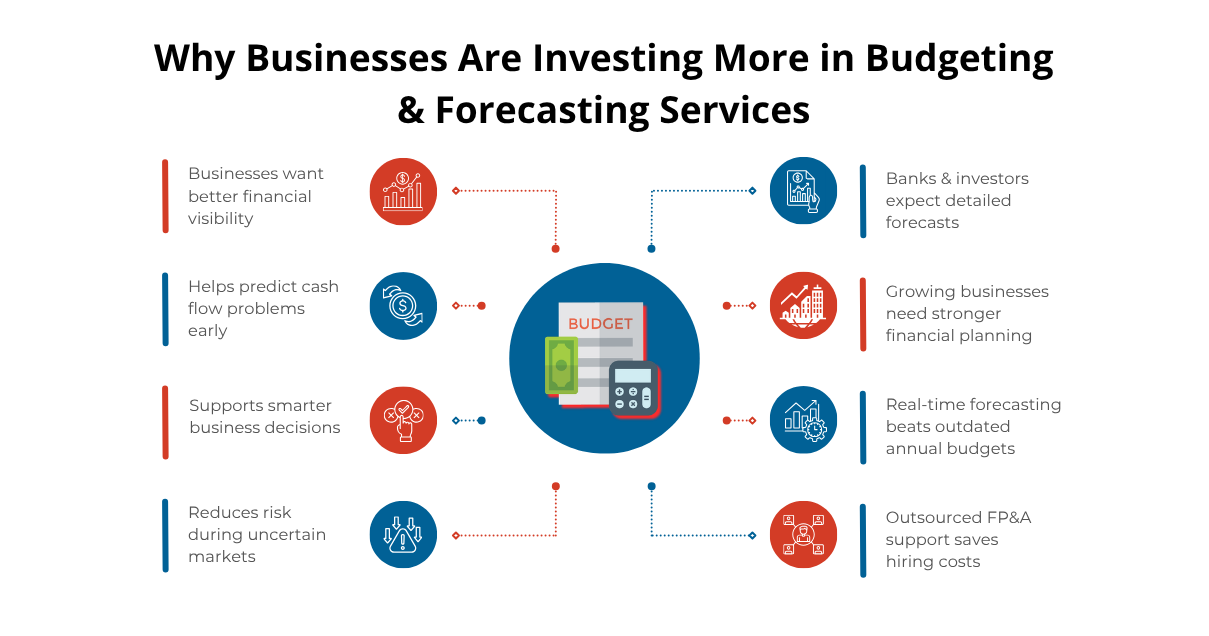

What’s changed recently is who’s buying these services. It used to be that serious financial planning was mostly a large-company concern. Smaller businesses either couldn’t afford it or figured they were too small to need it. That thinking has shifted quite a bit. The tools have become more affordable, the stakes have gone up, and frankly, the consultants in this space have gotten better at packaging what they offer into engagements that make sense for businesses that aren’t running $100 million in revenue.

A decent chunk of the growth in this market right now is coming from the SMB segment, particularly in the US, UK, and Australia, where business owners who’ve been through a rate cycle or two have come out the other side with a much clearer appreciation for what proper forecasting can do.

There’s a version of this answer that sounds like a press release. Interest rates, supply chain uncertainty, shifting consumer behavior. All true, all relevant. But the more honest answer is a bit more direct.

Businesses are paying for these services because the last few years genuinely rattled a lot of people. The businesses that came out of 2020-2022 in reasonable shape were, in a lot of cases, the ones with decent financial visibility. They knew their cash position. They had modeled out what a 20% revenue drop would do to them. They could see a problem developing three months before it became a crisis, which gave them time to do something about it.

The businesses that struggled were often the ones running on gut feel and annual budgets. When things moved fast, they had no real-time picture of where they stood.

That’s not an abstract observation. It’s something that showed up repeatedly in conversations between advisors and their clients during that period, and it’s left a lasting impression. The demand for professional financial modeling and strategic financial planning went up, and it hasn’t really come back down.

There’s also something worth saying about what lenders and investors expect now. If you’re going to a bank in Australia or the UK to refinance your commercial property or extend a credit facility, a rough set of projections on a spreadsheet isn’t going to cut it. They want to see a proper cash flow forecast, some scenario work, and evidence that management actually understands the numbers. That expectation has raised the bar for a lot of businesses that never previously needed to think about this level of detail.

And for businesses that are raising from private equity or venture capital, the standard is even higher. Investors in the US market, especially, are asking for rolling forecast models and monthly reforecasts, not the annual budget that was locked in before anyone knew what Q3 would look like.

The other thing driving it is the gap in most finance teams. Most growing businesses don’t have a proper FP&A function. They’ve got an accountant handling compliance, maybe a bookkeeper, and someone doing payroll. Nobody’s actually building a forward-looking financial model, because nobody has the time or the skill set. Bringing in an outside firm to handle that fills a real gap without the cost of a full-time strategic hire.

Revenue is what people talk about. Cash flow is what keeps the lights on.

Most experienced operators know this already, but it’s still worth saying clearly: businesses with healthy revenue can and do run into cash flow crises. A fast-growing business that’s extending longer payment terms to customers while paying its suppliers on shorter terms is often in a precarious position even while its P&L looks fine. Cash flow management consulting exists, in large part, to catch these situations before they become emergencies.

A proper cash flow forecast does a few things well. It shows you, months in advance, when your cash position is going to be under pressure. That lead time is the difference between having options and having no options. If you can see a shortfall coming in Q3, you can have a conversation with your bank about a credit facility in April. If you find out about it in August, you’re negotiating from a much weaker position.

Good cash flow modeling also surfaces the interplay between different parts of your working capital cycle. Your accounts receivable collection performance, your payroll timing, your supplier payment terms, your inventory holding position. These interact in ways that aren’t always obvious until you’ve actually built a model that connects them. Businesses that do this work regularly tend to have a much more mature relationship with their working capital, and that shows up in their financing costs and their negotiating position with suppliers and customers alike.

For any business going through a capital raise or a lending conversation, having a clean, well-built cash flow model is essentially table stakes now. In the US and UK markets particularly, the expectation from sophisticated investors and lenders is that management can walk them through a 13-week cash flow as well as a 12-month model with scenario overlays. Businesses that can’t produce that, or that produce it and clearly don’t understand the numbers behind it, face a harder conversation than those that have this as a standard part of their financial management process.

The phrase “data-driven decision making” gets used so often that it’s almost lost its meaning, so it’s worth being specific about what it actually looks like in a well-run financial planning function.

The traditional budgeting approach works roughly like this: take last year’s numbers, apply some growth assumptions, get sign-off from department heads, lock the budget, and then measure against it at year-end. The problem is that most of those growth assumptions are disconnected from the things that actually drive the business. They’re accounting-based rather than operationally-based.

Driver-based budgeting takes a different approach. Instead of saying “revenue will be $10M next year,” you build up from the operational drivers: how many customers do you expect, what’s your average deal value, what’s your expected churn rate, how many salespeople do you have and what’s their average productivity. The budget becomes a function of those drivers, which means when a driver changes, you can immediately see the financial impact and update the plan accordingly.

This is meaningfully more useful than a static budget. It gives you a model that you can actually use in real-time as the business evolves, not just an annual document that becomes irrelevant by March.

Integrated business planning (IBP) takes this further by connecting the financial plan to operations, supply chain, and sales planning within a shared set of assumptions. For businesses of a certain size, this kind of integration transforms financial planning from a finance function activity into something the whole business operates around.

Real-time financial dashboards that pull live data from your accounting system and display it against the plan are another piece of this. When your CFO or CEO can see on a Wednesday morning where the business is tracking against plan for the month, rather than waiting for the month-end report three weeks later, the quality of decisions improves. Problems get caught earlier. Opportunities get acted on faster.

This is where predictive financial models and the tools that support them have the most practical impact. It’s not that the models are predicting the future with certainty. It’s that they’re giving leadership a much cleaner read on what’s likely, what’s at risk, and what levers they can pull. That information, acted on quickly, compounds over time into meaningfully better business outcomes.

This section could easily turn into a hype piece, so let’s keep it grounded.

Artificial intelligence and machine learning have genuinely changed the speed and depth of what’s possible in financial forecasting. That’s real. Running 50 different revenue scenarios that used to take a senior analyst two days now takes a few minutes on a modern FP&A platform. Models can pull live data from your CRM, your accounting software, your inventory system, and your payroll platform simultaneously, which means your forecast is actually connected to what’s happening in the business rather than being based on manual inputs that are already three weeks old by the time the CFO looks at them.

Predictive financial models built on machine learning can identify patterns in historical data that are genuinely hard to spot manually. Seasonality patterns, cost drivers, the relationship between marketing spend and revenue on a lag, things that get buried in a standard Excel model but surface quickly when you’ve got the right analytical tools running on clean data.

There are also tools now that handle what-if analysis in a way that’s actually practical for non-finance people to use. A business owner can run “what happens to my cash position if my biggest client pays 45 days late and my material costs go up 8%?” and get an answer in a few minutes. That kind of accessibility has changed how leaders engage with their financial data.

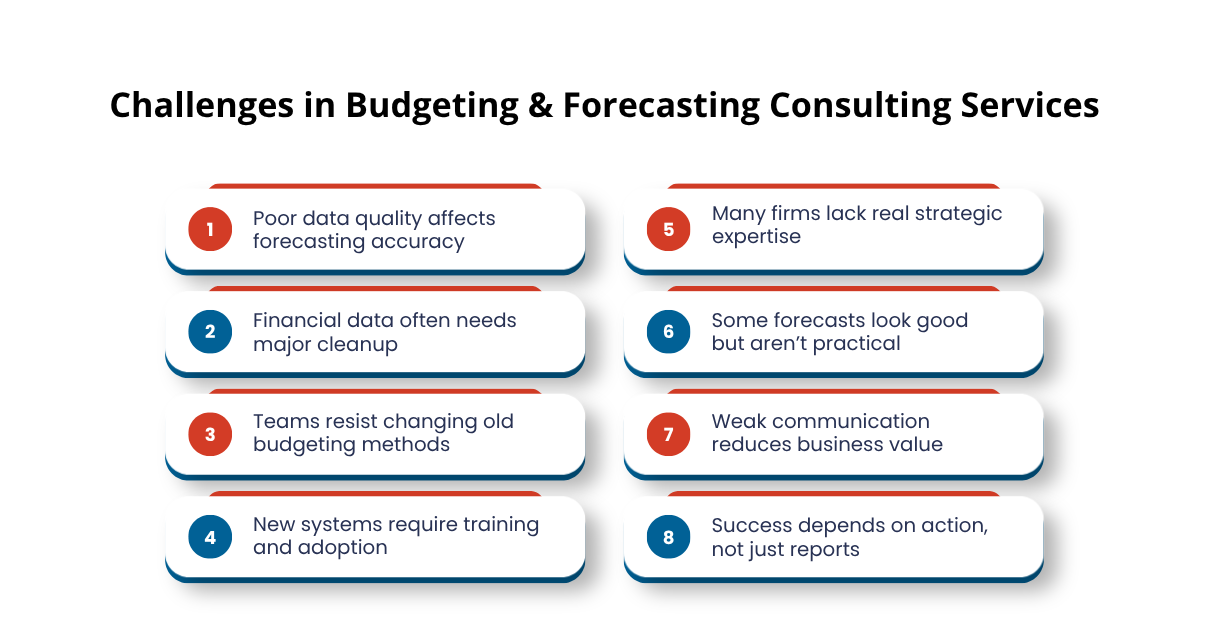

But here’s the thing that gets underplayed in most coverage of this: AI in forecasting is only as good as the data and the judgment behind it. A lot of businesses that have tried to adopt these tools have run into the same wall. The data coming out of their accounting system is inconsistent, their chart of accounts is a mess, and nobody’s set up the integrations properly. The tool sits there looking impressive and producing garbage outputs because the inputs were never right.

The consultants who are genuinely adding value in this area aren’t just the ones who know the software. They’re the ones who can come in, sort out the data foundation, configure the model properly, and then actually explain to the leadership team what the outputs mean and where they should push back on the numbers. That judgment layer is still entirely human, and it’s where a lot of the consulting value lives.

Excel gets a bad reputation that’s partly unfair. For a lot of businesses, a well-built Excel model is perfectly adequate for where they are. The problems show up when the business grows past a certain point and the spreadsheet stops scaling gracefully. Version control becomes a nightmare. Multiple people can’t work in the same model simultaneously. The links between tabs break. Someone overwrites a formula and nobody notices until the board meeting.

Cloud-based financial planning and analysis (FP&A) platforms solve those specific problems, and for businesses that are past the point where Excel is working well, the shift is usually worth it.

The main platforms in this space, Anaplan, Workday Adaptive Planning, Vena, Planful, and a few others, offer genuine improvements over spreadsheet-based planning in a few key areas. Real-time collaboration, so the sales team and the finance team can work on assumptions simultaneously without creating conflicting versions. Automated data feeds that pull from accounting, ERP, and CRM systems so the forecast is always working with current numbers. Audit trails that show every change and who made it, which matters more than most people realize when you’re doing a board presentation and someone asks why a number moved.

The scenario modeling capability in these platforms is also genuinely better than what most Excel models can manage practically. You can store multiple versions of a forecast, run sensitivity analysis across different assumptions simultaneously, and share a clean view of the outputs with people who don’t need to see the underlying model.

The adoption of these tools has created a secondary market in the consulting space. Businesses don’t just need help with the financial strategy side; they need help selecting the right platform, configuring it properly, integrating it with their existing systems, and training their team to use it. Consultants who can do both the strategy work and the implementation work are in meaningful demand.

The virtual CFO model has been around for a while, but it’s grown into something meaningfully different over the last few years, and it’s now one of the more interesting parts of the budgeting and forecasting consulting services market.

The basic idea is straightforward enough. A business that’s too small to justify paying a CFO $250,000 a year still needs CFO-level thinking. So instead of hiring someone full time, they bring in a firm or an individual on a part-time or fractional basis to provide that strategic financial leadership.

Where it gets interesting is what this model actually looks like in practice for a business in the $5M to $30M revenue range in the US or Australia. The engagement typically starts around getting the financial planning function into some kind of workable shape: building a proper 12-month forecast, setting up a monthly reporting cadence, connecting the budget to the operational numbers that actually matter.

From there it tends to grow. The vCFO ends up in the room for key decisions, whether it’s a capital raise, a major hire, a new market entry, or a pricing decision. They’re running budget vs. actual reviews each month, explaining to the founder or CEO what the variances mean and what they suggest about where the business is heading. They’re building the key performance indicators (KPIs) that give management a real-time read on financial health rather than waiting for month-end accounts.

This model works well in the UK and New Zealand too, partly because the geography is no longer a barrier. Most of these engagements are now run entirely remotely, which means a business in Auckland or Manchester can access the same quality of financial advisory support as one in Sydney or Chicago. The tools make that practical in a way that wasn’t really possible ten years ago.

One thing worth noting: the businesses that get the most from a vCFO engagement tend to be the ones where the founder or CEO genuinely engages with the financial data. If the monthly forecast review turns into a formality that nobody reads, the value drops considerably. The firms that deliver well in this space invest time in making sure their clients actually understand and use what’s being built for them.

Data quality is the single biggest issue. The promise of AI-powered forecasting and automated dashboards runs straight into the reality that most businesses are sitting on years of messy financial data: inconsistent categories, transactions booked in the wrong accounts, integrations between systems that have never worked properly. Before any sophisticated forecasting can happen, there’s usually a cleanup project that nobody budgeted for and nobody’s particularly excited about doing. Consultants who manage expectations around this upfront save themselves a lot of difficult conversations later.

The change management side of these projects also gets underestimated. Replacing a finance team’s existing process, even a bad one, requires genuine buy-in. People who have been building the budget in Excel for five years are not automatically enthusiastic about learning a new platform. If the implementation doesn’t address the human side of the change alongside the technical side, adoption tends to be shallow and the promised benefits don’t materialize.

There’s also a quality problem in the consulting market itself. The growth in demand has attracted a lot of providers, and the gap between the best and the worst is significant. The best firms combine real financial modeling expertise with industry knowledge, commercial judgment, and the ability to communicate clearly with people who are not accountants. That combination is genuinely uncommon. The weaker end of the market is good at building models but not at connecting those models to the actual decisions a business needs to make.

Clients contribute to the problem too. Some businesses engage a consulting firm for a forecasting project with the implicit expectation of getting a document that looks good rather than a process that works. When the deliverable is a polished forecast that nobody in the business actually updates or acts on, the engagement has produced something close to zero value despite looking successful on paper. The best consultants push back on this dynamic, which isn’t always comfortable, but it’s what separates good advisory relationships from expensive box-ticking.

The continued integration of AI into financial planning and analysis processes seems inevitable. The tools will get better, the interfaces will become easier to use, and the automation of routine data work will free up consultants and in-house teams to spend more time on the interpretation and judgment work that actually drives decisions. That’s probably a good development overall, though it will change what clients need from their advisors and what skills command a premium.

Real-time financial reporting is going to become a standard expectation rather than a differentiator. Right now, businesses that have live dashboards connected to their accounting systems and a forecast that updates weekly are ahead of the curve. In three to five years, that will just be normal. The businesses that are still running on monthly spreadsheets will be at a noticeable disadvantage, particularly when they’re trying to attract investment or access financing.

The outsourced FP&A model will keep growing. The talent market for senior finance professionals is competitive, and the cost of building a proper in-house FP&A function is substantial. For businesses below a certain size threshold, outsourcing that function to a firm that specializes in it will continue to make more financial sense than hiring for it. That’s been the trend, and nothing on the horizon suggests it reverses.

ESG reporting is becoming increasingly relevant to financial planning for businesses with institutional customers or investors. Requirements to report on environmental and social metrics are already standard in many larger organizations in the UK and Australia, and the expectation is filtering down to smaller businesses through supply chain and investor requirements. Consultants who can integrate non-financial data into planning frameworks alongside the traditional financial metrics will be better positioned than those who treat it as a separate, unrelated activity.

The one genuinely uncertain thing is how AI tools will change the competitive dynamics of the consulting market itself. If the analytical work becomes substantially automated, the firms that compete on model-building skills alone will face pricing pressure. The ones that compete on judgment, relationships, and the ability to connect financial analysis to business strategy will likely hold their value better. That distinction has always mattered. It’s going to matter more.

Indian Muneem Chartered Accountant (IMCA) works with businesses in the US, UK, Australia, and New Zealand across the full range of what good financial planning actually requires.

The starting point is always understanding how a specific business works, not applying a generic template. A professional services firm with lumpy project revenue and a manufacturing business with complex inventory cycles need quite different approaches to forecasting, even if the underlying methodology shares common principles. Getting that context right before building anything is most of the work.

From there, the IMCA team builds the financial planning infrastructure that fits where the business actually is. For some clients, that’s a clean, well-structured budget with a rolling forecast model that the in-house team can maintain. For others, it’s implementing a cloud FP&A platform properly, including the integrations with accounting software and the training to make sure the team uses it well. For clients with more complex needs, it extends into ongoing virtual CFO support: monthly forecast reviews, board reporting, cash flow oversight, and having a senior financial mind available when significant decisions are being made.

The cash flow modeling work IMCA does tends to be particularly valued by businesses that are growing quickly or going through a capital raise, because those are the situations where cash position visibility matters most. A clear 13-week cash flow alongside a 12-month model with proper scenario overlays is something most banks and investors expect and most businesses struggle to produce without outside help.

The broader goal across all of it is that the business ends up with financial planning that actually informs how it operates, not just a set of documents that satisfy a compliance requirement.

The businesses that take financial planning seriously tend to outperform the ones that don’t. That’s not a controversial claim. What’s changed is that the bar for what “taking it seriously” looks like has risen, and the tools and services available to meet that bar have improved significantly.

The budgeting and forecasting consulting services market reflects a shift in how businesses across the US, UK, Australia, and New Zealand think about financial visibility. Not as a compliance exercise, not as an annual ritual, but as an ongoing function that informs real decisions in close to real time.

Whether that means building a proper rolling forecast, shifting from Excel to a cloud FP&A platform, bringing in a virtual CFO to own the financial planning function, or just getting a genuinely useful cash flow model built for the first time, the direction is clear. Better financial planning produces better outcomes. The market exists because that’s true, and it’s growing because more businesses are figuring that out.

We use cookies and similar technologies to improve your experience, personalise content, and analyse traffic. Some are essential for access to our products and informational resources. Certain services or pages may also be governed by additional Terms of Use. Manage your preferences at any time.