Xero vs QuickBooks: Country-Wise Comparison (2026) – Which Accounting Software Is Right for Your Business?

Table Of Contents

Toggle

Here’s something that catches a lot of businesses off guard when they start selling internationally: GST and VAT aren’t the same thing, even though they look nearly identical from a distance. Both are consumption taxes. Both use input credits. Both hit the end consumer. But the way they’re structured, administered, and applied varies enough that what works in one country can create real compliance headaches in another.

If you’re selling into the UK, New Zealand, Australia, or across Europe, the differences between GST and VAT will show up in your operations whether you plan for them or not. Better to understand them now.

Both taxes collect revenue at each point in the supply chain. A supplier charges tax on a sale, the buyer reclaims it through input tax credits, and the net amount flows to the government. The end consumer pays the full accumulated tax with no right of recovery.

That’s the shared foundation. Where countries diverge is in how they build on top of it. Some keep the system lean with a single rate and a broad base. Others stack on multiple rates, exemptions, and special categories until compliance becomes its own industry.

The differences between GST and VAT become a real operational issue the moment you’re dealing with more than one country. And for global businesses, that’s usually from day one of international expansion.

VAT is common in EU nations, the United Kingdom, and about 160 countries around the world. At every step in the value chain, organizations levy output VAT on sales, credit input VAT to purchases, and pay out the net amount.

The problem lies with the structure of the rates, as different nations have different rates. For instance, the UK VAT system includes three types of rates, which include standard at 20%, reduced at 5%, and nil VAT rate for such goods as food products and kid’s clothes. In Germany, there is standard rate at 19% and reduced rate at 7%.

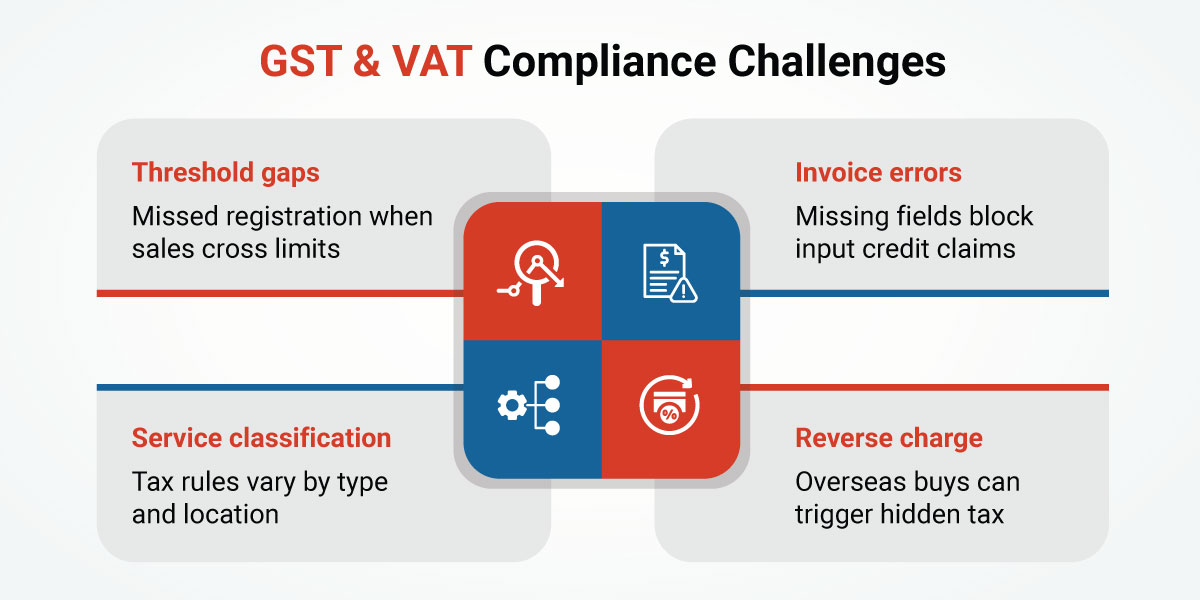

A tax invoice in France needs specific fields that may differ from what Germany requires. Miss one, and your input VAT claim is at risk. Multiply that across several EU markets and you start to see the scale of the compliance management involved.

The reverse charge mechanism shifts the VAT obligation in B2B cross-border services from the supplier to the buyer. For international businesses selling services into the EU, this is one of the most important rules to understand and one of the most commonly missed.

Goods and Services Tax works on the same input credit model, but countries that built GST systems more recently tended to design out the complexity that VAT accumulated over decades.

New Zealand’s GST is the best example. One rate, 15%, applied to almost everything. Minimal exemptions. Administered centrally by the Inland Revenue Department. Businesses know what applies and what doesn’t without needing a specialist on retainer.

Despite having a federal GST rate of 5%, provinces impose their sales tax or HST (harmonized sales tax), which makes Canada more complicated compared to Australia or New Zealand, even though they have GST in common.

For foreign suppliers, Australia and New Zealand demand that non-residents register under GST if they reach local turnover limits for digital goods and services provided. New Zealand expanded this requirement in 2016, while Australia did so in 2017.

The US runs on state-level sales tax, applied only at the final point of sale to the consumer. No input credit system. No multi-stage collection. A business that pays sales tax on raw materials cannot reclaim it; it becomes a cost.

Rates vary wildly. Oregon has none. Combined state and local rates in some Louisiana parishes exceed 10%. What’s taxable varies too. Some states tax digital services, some don’t. Some exempt groceries, some don’t.

There’s no national consumption tax in the US because the political conditions for one don’t exist. Federal revenue comes from income and payroll taxes. A national VAT would require renegotiating the relationship between federal and state taxation, which nobody in Washington is interested in doing.

What changed the picture for international businesses was South Dakota v. Wayfair in 2018. Before that, no physical presence generally meant no sales tax obligation. After Wayfair, sales volume alone creates economic nexus. A foreign business selling into the US can now have filing obligations in multiple states without a single employee on US soil.

This is what global businesses actually need to know.

Rate structure: VAT systems in Europe commonly have three or more rates. GST systems, particularly in New Zealand and Australia, use one or two. Fewer rates mean fewer classification disputes. The UK famously spent years litigating whether a particular chocolate biscuit was a cake (zero-rated) or a biscuit (standard-rated). That kind of thing doesn’t happen in New Zealand.

Administration: EU VAT is fragmented. Each member state is its own authority with its own processes. GST in Australia and New Zealand is one authority, one system. For a finance team managing international compliance, that’s a significant difference in workload.

Thresholds for Registration: The registration threshold in Australia is AUD 75,000 per annum, while in New Zealand, it stands at NZD 60,000. In the case of the European Union, it differs from state to state; however, with the recent 2021 reformations in e-commerce, there now exists a universal threshold of EUR 10,000.

Exemptions and scope: Because GST systems tend to have fewer exemptions, the tax base is wider. New Zealand’s 15% GST raises strong revenue precisely because almost nothing escapes it. European VAT systems narrow the base with exemptions while applying higher headline rates.

Cross-border digital services: Both systems now cover outsourced digital sellers, but through different mechanisms. The EU uses the One Stop Shop (OSS) scheme to consolidate filings across multiple countries for businesses selling B2C. Australia and New Zealand require direct registration with their respective authorities.

| Factors | GST | VAT | US Sales Tax |

| Collection | Multi-stage | Multi-stage | Retail only |

| Input credit | Yes | Yes | No |

| Rates | Usually one | Multiple tiers | Varies by state |

| Administration | Central | Fragmented (EU) | 50+ state systems |

| Consumer bears cost | Yes | Yes | Yes |

The standout difference with US sales tax is the absence of input credits. Businesses at intermediate stages of production actually absorb embedded tax, which VAT and GST specifically avoid.

Compliance simplicity is real. One rate, broad base, one authority. A business entering New Zealand or Australia can build a functional GST compliance process without a specialist tax team. That’s not true of entering five EU markets simultaneously.

Fewer exemptions also mean fewer classification disputes. Businesses don’t spend money arguing about which rate applies. They know the rate, they charge it, they file.

The wider tax base means revenue is maintained at lower rates. That’s good policy design, and it’s why economists generally favor the GST model over the multi-rate VAT approach.

VAT also has decades of established case law, compliance infrastructure, and mature accounting systems behind it. Businesses that know the EU VAT system can operate efficiently within it. The OSS scheme has meaningfully reduced multi-country compliance burden for digital sellers.

US businesses going international face the steepest adjustment. The input credit concept is foreign to US accounting practice. EU VAT’s fragmentation across member states is consistently underestimated. New Zealand and Australia are more accessible entry points, with cleaner GST systems and straightforward registration processes for outsourced sellers.

Threshold monitoring is the most common gap. Businesses hitting new markets often don’t track when they cross registration thresholds, especially if the sales team and finance team aren’t communicating.

Cross-border service classification is genuinely hard. Whether a service is taxable, where it’s taxed, and who accounts for it depends on the transaction type, the location of the parties, and the specific rules of each jurisdiction.

On systems: tax compliance platforms like Avalara or Thomson Reuters ONESOURCE handle rate lookups, threshold monitoring, and filing preparation. Once you’re operating across more than two or three countries, the manual approach doesn’t hold up.

On people: local advisors matter because rules change. EU VAT updates, ATO rulings, IRD guidance, none of it is static. A local advisor in each key market catches changes before they become compliance failures.

On process: someone needs to own cross-border tax compliance. Not shared ownership between finance and legal. Actual ownership, with visibility into sales by jurisdiction and a clear process for triggering registration when thresholds are hit.

Use simplification schemes where they exist. The EU’s OSS for B2C digital sales is worth using. It’s not perfect, but it reduces the number of separate national VAT registrations significantly.

Plan for refund timing. Businesses that export heavily often accumulate VAT and GST refund positions because exports are typically zero-rated. In some countries, refunds take months. That’s a working capital issue worth modeling in advance.

GST versus VAT distinctions will come up during your business operations regardless of whether or not you expect them to happen. The successful companies who know how to deal with such situations are those who understand compliance as a structural problem and develop their necessary systems and relationships beforehand.

Indian Muneem Chartered Accountant handles your GST and VAT end to end, from transaction data through to lodgement, reconciliation, deadline monitoring, and audit-ready documentation. No chasing. No gaps. No surprises when rules change.

We use cookies and similar technologies to improve your experience, personalise content, and analyse traffic. Some are essential for access to our products and informational resources. Certain services or pages may also be governed by additional Terms of Use. Manage your preferences at any time.