Xero vs QuickBooks: Country-Wise Comparison (2026) – Which Accounting Software Is Right for Your Business?

Table Of Contents

Toggle

Numbers don’t lie, but they do hide things. Especially when the person entering them is stretched thin, working off a system nobody properly set up, or just assuming the software will catch what they miss. It won’t.

Financial reporting mistakes are far more common than most business owners admit, and they rarely look catastrophic at first. They look like a slightly off-balance sheet. A revenue figure that seems a bit high. A tax return that takes longer than usual to file because the bookkeeper keeps finding things that don’t add up.

By the time the real damage shows up, it’s usually been building for months.

This isn’t a beginner’s guide to what a balance sheet is. If you’re reading this, you probably already know that. What this covers is where experienced, well-intentioned businesses still get it wrong, and what actually fixing it looks like in practice.

You already know the basics. Financial reporting is how a business communicates its financial position to the people who need to know, whether that’s investors, lenders, tax authorities, or simply the founder of a company trying to understand why profit is good, but there’s no money in the bank.

The main financial reports are: the income statement, the balance sheet, and the cash flow statement. These three reports, collectively, are “supposed to” give a clear, honest picture of a business’s financial situation.

The word “supposed to” is doing a lot of work in that sentence.

You delay decisions. You make assumptions that turn out to be wrong because they were based on data that was wrong first.

That’s the real cost of poor reporting. Not just the compliance risk, though that’s real too. It’s the slow erosion of your ability to trust what you’re looking at.

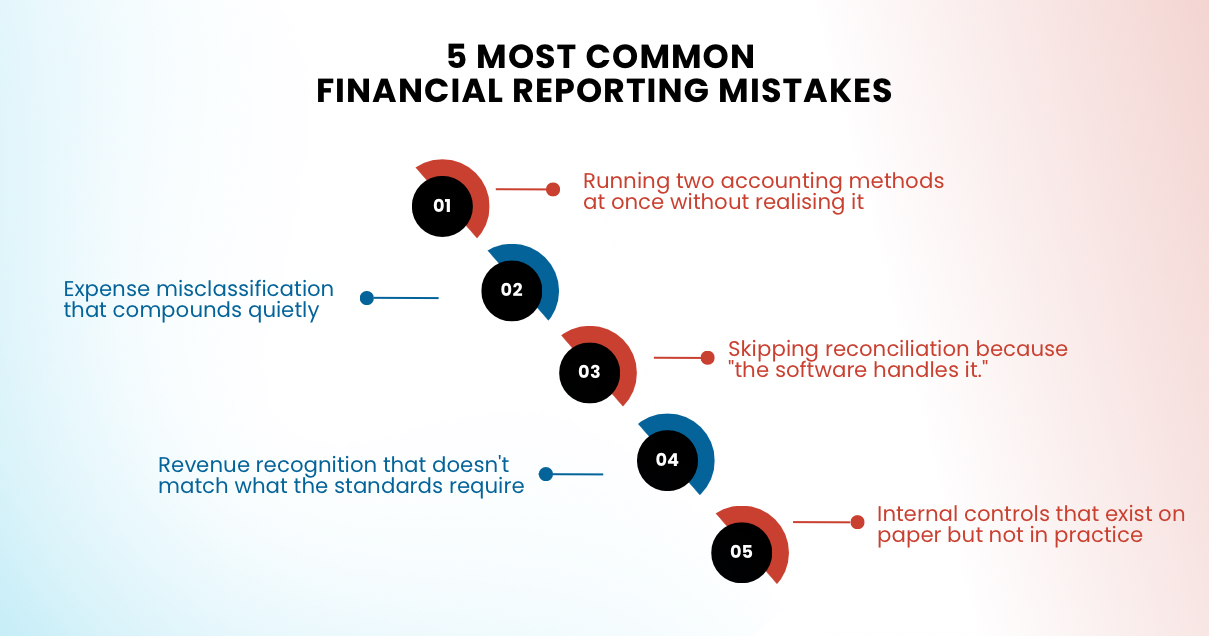

This one is surprisingly easy to do and genuinely difficult to spot once it’s embedded.

Cash basis accounting and accrual accounting are not interchangeable. Cash basis records transactions when money moves. Accrual records them when they’re earned or owed, regardless of when the cash actually arrives. Both are legitimate. Mixing them is not.

The typical version of this mistake looks like: revenue gets recorded when invoices are paid (cash), but expenses get recorded when bills arrive (accrual). It feels logical in the moment. It produces a profit and loss statement that doesn’t actually reflect reality.

The fix isn’t complicated. Pick one method and apply it consistently across everything. If your business carries outstanding invoices or has bills sitting unpaid at any given time, accrual accounting will give you a far more accurate picture of where you actually stand. If you’re unsure which method you’re currently using, that uncertainty is itself the answer.

A meal gets coded as marketing. A piece of equipment goes into operating expenses instead of capital expenditure. A personal subscription sits quietly in the business accounts.

None of these look like disasters individually. Over time, they distort your operating expenses, skew your net income, and affect how much tax you owe. They can also put you at odds with GAAP or IFRS requirements, depending on your market and the nature of your reporting obligations.

The businesses that manage this well don’t have smarter people. They have a clear chart of accounts that everyone on the team actually understands, with rules set up in their accounting software so recurring transactions land correctly without anyone having to think about it each time. They also run periodic reviews, not once a year at tax time, but quarterly, to catch drift before it stacks up.

Bank reconciliation is the part of the process that a surprising number of growing businesses quietly stop doing properly once they get busy. The logic is understandable: the accounting platform pulls in the bank feed automatically, transactions get matched, it looks fine.

It is not fine if nobody is actually checking the output.

Duplicate entries, bank fees that never got recorded, transactions that matched incorrectly, payments that went out but didn’t get categorised these all slip through automated systems. The gap between what your books show and what’s actually in your accounts widens slowly. Then you hit a financial statement analysis review, or worse, an audit, and the cleanup takes weeks.

Reconciliation should happen monthly at a minimum. The software does the matching. A human still needs to look at the exceptions and confirm that the result is correct.

This one gets messier the more complex your revenue model is. Subscriptions, long-term service contracts, software licences with implementation components, bundled offerings, all of these create revenue recognition questions that a simple invoice date doesn’t answer.

Under IFRS 15 (and ASC 606 for US-based businesses), revenue gets recognised when a performance obligation has been satisfied. Not when the contract is signed. Not when the deposit clears. When the thing you promised to deliver has actually been delivered.

The practical version of fixing this isn’t about building a corporate compliance department. It’s about identifying the two or three places in your process where an error or manipulation could go undetected, and making sure at least one other person is looking at those points regularly.

Most mistakes surface through one of three routes: a monthly close process that’s done properly, an internal review that’s actually thorough, or an external audit that finds what everyone else missed.

If you want to catch errors early, the monthly close is your best tool. It should include a reconciliation of every account, a comparison of line items against prior periods to flag anything that looks unusual, a clean trial balance, and ideally a review of key reports by someone who didn’t prepare them.

For corrections, timing matters. An error in the current period is usually straightforward to fix with a journal entry and a note in the records. An error from a prior period that materially affected your financial statements is a different situation, it may need to be restated and disclosed, which is a more involved process that affects multiple stakeholders.

The common thread is speed. Errors that get caught in the month they happen are almost always cheaper to fix than errors discovered a year later during a tax audit.

Bad numbers lead to bad decisions. If your margins look healthier than they are, you scale prematurely. If your cash flow looks worse than it is, you pass on hires or investments that would have paid off. The decisions feel reasonable at the time because they’re based on data. But the data was wrong.

For companies with external investors or active lenders, inaccurate financial reporting creates a different kind of exposure. It damages trust in a way that’s very hard to rebuild once it’s gone. Most sophisticated investors have seen enough to know when numbers don’t quite add up, and when they start asking questions, the conversation gets uncomfortable fast.

In the US, the Securities and Exchange Commission (SEC) oversees reporting for public companies, with standards governed by the Financial Accounting Standards Board (FASB). Private companies have more flexibility but still operate within GAAP expectations, particularly when dealing with institutional lenders or investors.

In the UK, the Financial Reporting Council (FRC) sets accounting standards and audit requirements. In Australia, that role falls to the Australian Accounting Standards Board (AASB). In New Zealand, the External Reporting Board (XRB) governs standards, both aligned broadly with IFRS.

For most small and mid-sized businesses not listed on a public exchange, direct interaction with these regulators is limited. But tax authorities in all these markets expect your financial records to be accurate and consistent, and the standards these bodies set are often what your accountant or lender will hold you to anyway.

Technology reduces errors when it’s set up correctly and reviewed regularly. It multiplies errors when it isn’t. Setting up your platform properly at the start, with someone who actually knows what they’re doing, is one of the better investments a growing business can make.

For businesses with cross-border operations, this becomes more important. The rules around deferred tax, depreciation methods, and intercompany transactions vary by jurisdiction, and the differences aren’t always intuitive. Getting this wrong in one market can create a compliance problem in another.

The businesses that outgrow financial problems are usually the ones that invested in professional support before those problems became serious.

Your month-end close takes longer than a week, and nobody is quite sure why. Your reports show consistent profit, but cash is always tighter than expected. You’ve had to amend a prior year’s tax return. A lender or investor has asked follow-up questions about specific line items, and the answers took longer than they should have.

The less obvious ones: your financial statements look almost identical month after month, even though your business is clearly changing. Nobody on your team can explain a particular number without going back to check. You’re not certain whether your accounting is on a cash or accrual basis.

Any one of these warrants a proper review. Financial reporting mistakes don’t announce themselves. They accumulate quietly, and the cost of ignoring them tends to grow faster than the cost of addressing them early.

Follow Us:

We use cookies and similar technologies to improve your experience, personalise content, and analyse traffic. Some are essential for access to our products and informational resources. Certain services or pages may also be governed by additional Terms of Use. Manage your preferences at any time.